NO.PZ2015121801000067

问题如下:

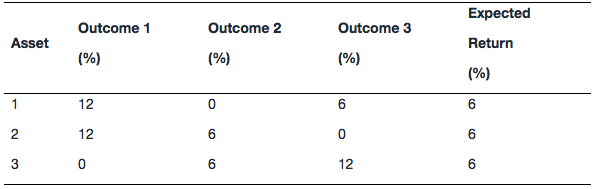

An analyst has made the following return projections for each of three possible outcomes with an equal likelihood of occurrence:

If the analyst constructs two-asset portfolios that are equally-weighted, which pair of assets has the lowest expected standard deviation?

选项:

A.

Asset 1 and Asset 2.

B.

Asset 1 and Asset 3.

C.

Asset 2 and Asset 3.

解释:

C is correct.

An equally weighted portfolio of Asset 2 and Asset 3 will have the lowest portfolio standard deviation, because for each outcome, the portfolio has the same expected return (they are perfectly negatively correlated).

1怎么看出来选项2和3是负相关的?在outcome2中,不都是6吗?难道看的是一个从小到大,另一个从大到小? 2我看之前提问的回答,这题目还能用计算器算?用的7~data,啥意思没毛病