NO.PZ201909280100001002

问题如下:

Which opportunistic hedge fund strategy meets Xu’s

preferences?

选项:

A.Only global macro

Both global macro and managed futures

解释:

C is correct. Xu

states that she prefers opportunistic hedge fund strategies that use high

leverage, have high liquidity, and exhibit right-tail skewness. The two most

common opportunistic hedge fund strategies are global macro and managed futures.

Both global macro and managed futures are highly liquid. Further, returns of

managed futures strategies typically exhibit positive right-tail skewness in

periods of market stress, whereas global macro strategies have delivered similar

diversification in such stress periods but with more heterogeneous outcomes. Global

macro and managed futures strategies can also use high leverage, either through

the use of futures contracts, in which high leverage is embedded, or through

the active use of options, which adds natural elements of leverage and positive

convexity.

A and B are incorrect

because both global macro and managed futures strategies can offer the three characteristics

that Xu seeks in an opportunistic hedge fund strategy.

C是正确的。 Xu表示,她更喜欢使用高杠杆、高流动性和右尾偏斜的 opportunistic hedge fund strategies。 两种最常见的 opportunistic hedge fund strategies是global macro and managed futures。 global macro and managed futures都具有高度流动性。 此外,managed futures的回报通常在市场压力时期表现出正的右尾偏度,而global macro在这种压力时期实现了类似的多样化,但结果更加heterogeneous outcomes(多样化)。global macro and managed futures也可以使用高杠杆,要么通过使用嵌入高杠杆的期货合约,要么通过积极使用期权,这增加了杠杆和正凸性的自然元素。

A 和 B 是错误的,因为全球宏观和管理期货策略都可以提供徐在机会主义对冲基金策略中寻求的三个特征。

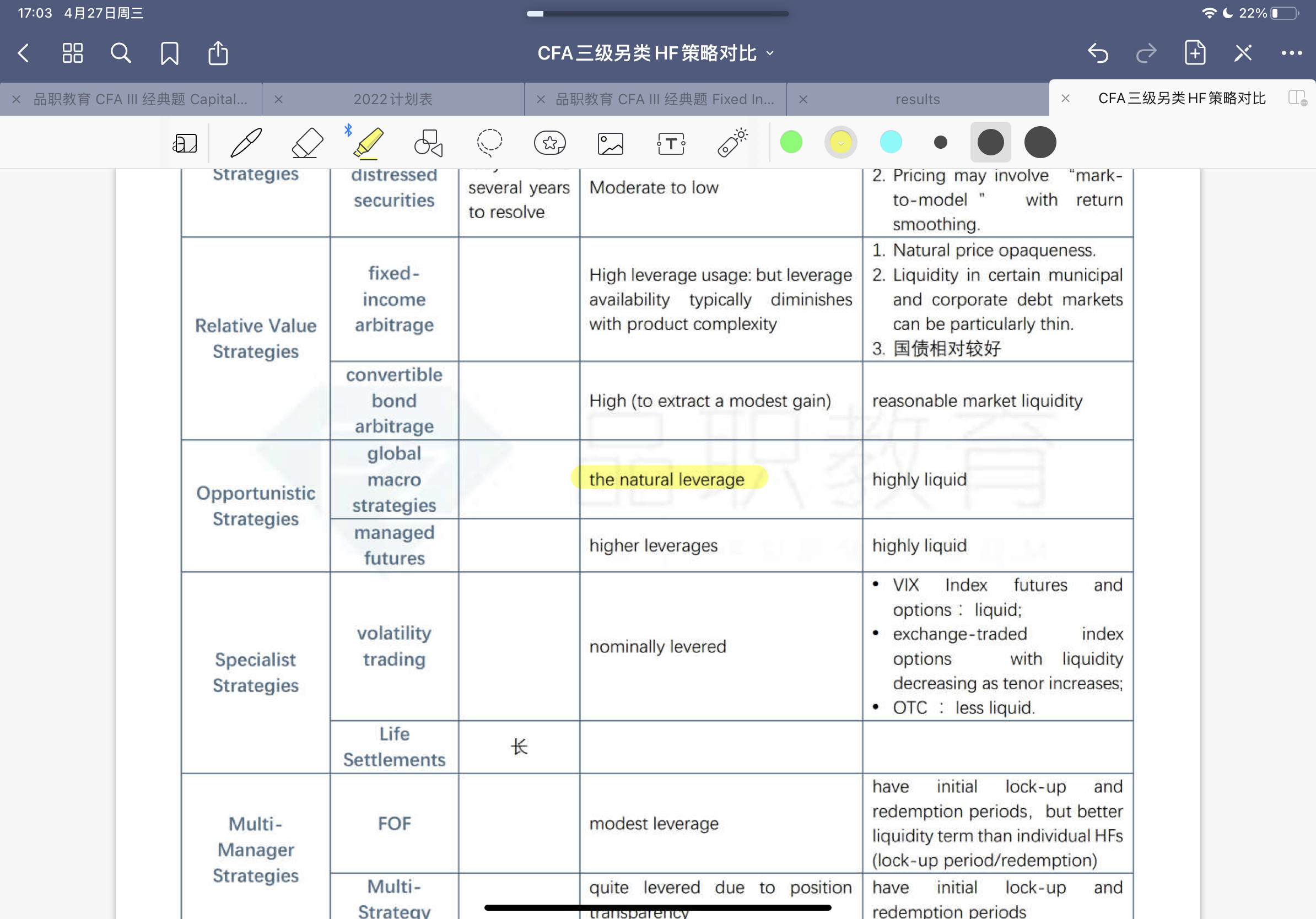

PS:global macro的右偏效果不明显,但是也有,但是和 managed futures的直接就是右偏不同,global macro 是因为在市场萧条时期的的多样化的表现(和实现萧条时其它资产都是左偏的不同)展示的右偏。这里看起来有些复杂,不要记混。原版书是这么解释的,我们答题也只能这个角度出发。

global macro volatility这么高,而且品职的总结表里写的是the natural leverage ‘