NO.PZ2018113001000053

问题如下:

Olivia, a fund manager, sells $50,000 vega notional of a one-year variance swap on the S&P 500 at a strike of 20% (quoted as annual volatility).

If the one-year realized volatility is 18%, the settlement amount at expiration of the swap for Olivia is:

选项:

A. pay $95,000 to the swap buyer.

B. receive $95,000 from the swap buyer.

C. receive $125,000 from the swap buyer.

解释:

B is correct.

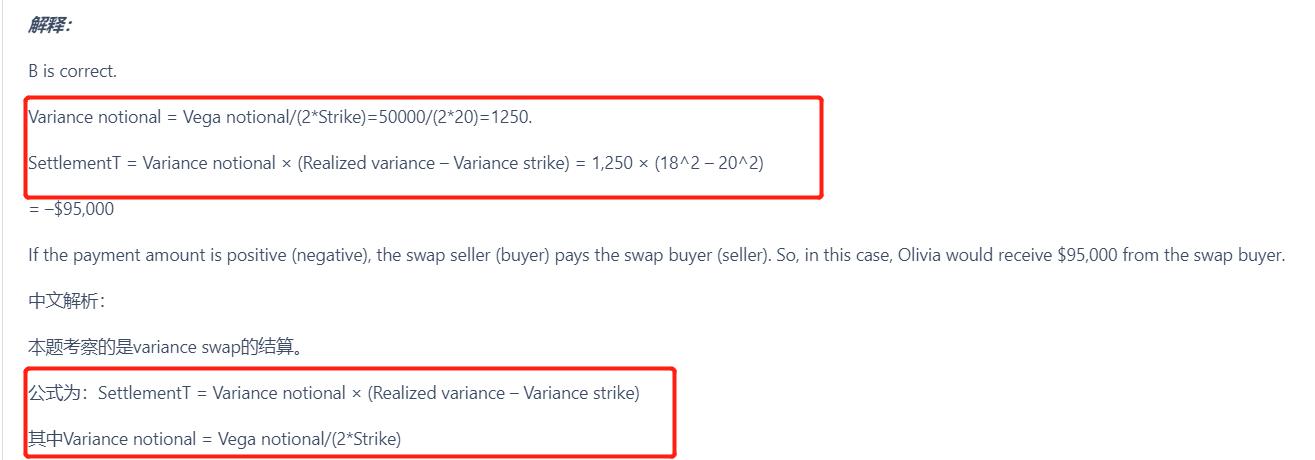

Variance notional = Vega notional/(2*Strike)=50000/(2*20)=1250.

SettlementT = Variance notional × (Realized variance – Variance strike) = 1,250 × (18^2 – 20^2)

= –$95,000

If the payment amount is positive (negative), the swap seller (buyer) pays the swap buyer (seller). So, in this case, Olivia would receive $95,000 from the swap buyer.

中文解析:

本题考察的是variance swap的结算。

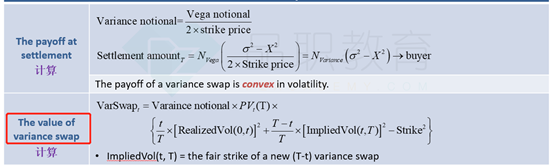

公式为:SettlementT = Variance notional × (Realized variance – Variance strike)

其中Variance notional = Vega notional/(2*Strike)

代入数字计算即可。

其中realized variance即σ2 ,variance strike 即X2

注意代入数字时,只取百分号前面的数字。

注意上述公式是站在long position的角度,如果结果为负数,说明是swap的买方要付给swap的卖方,本题问的是swap的卖方,因此seller是收到95,000

这个variance swap计算合约本金的公式在哪里