NO.PZ202108100100000206

问题如下:

From the bank’s perspective, based on Exhibits 6 and 7, the value of the 6 x 9 FRA 90 days after inception is closest to:

选项:

A.

$14,817.

B.

$19,647.

C.

$29,635.

解释:

A is correct.

The current value of the 6 × 9 FRA is calculated as

The 6 × 9 FRA expires six months after initiation. The bank entered into the

FRA 90 days ago; thus, the FRA will expire in 90 days. To value the FRA, the

first step is to compute the new FRA rate, which is the rate on Day 90 of an

FRA that expires in 90 days in which the underlying is the 90-day Libor:

Exhibit 7 indicates that L90 = 0.90% and L180 = 0.95%, so

herefore, given the FRA rate at initiation of 0.70% and notional principal of

$20 million from Exhibit 1, the current value of the forward contract is calculated as

中文解析:

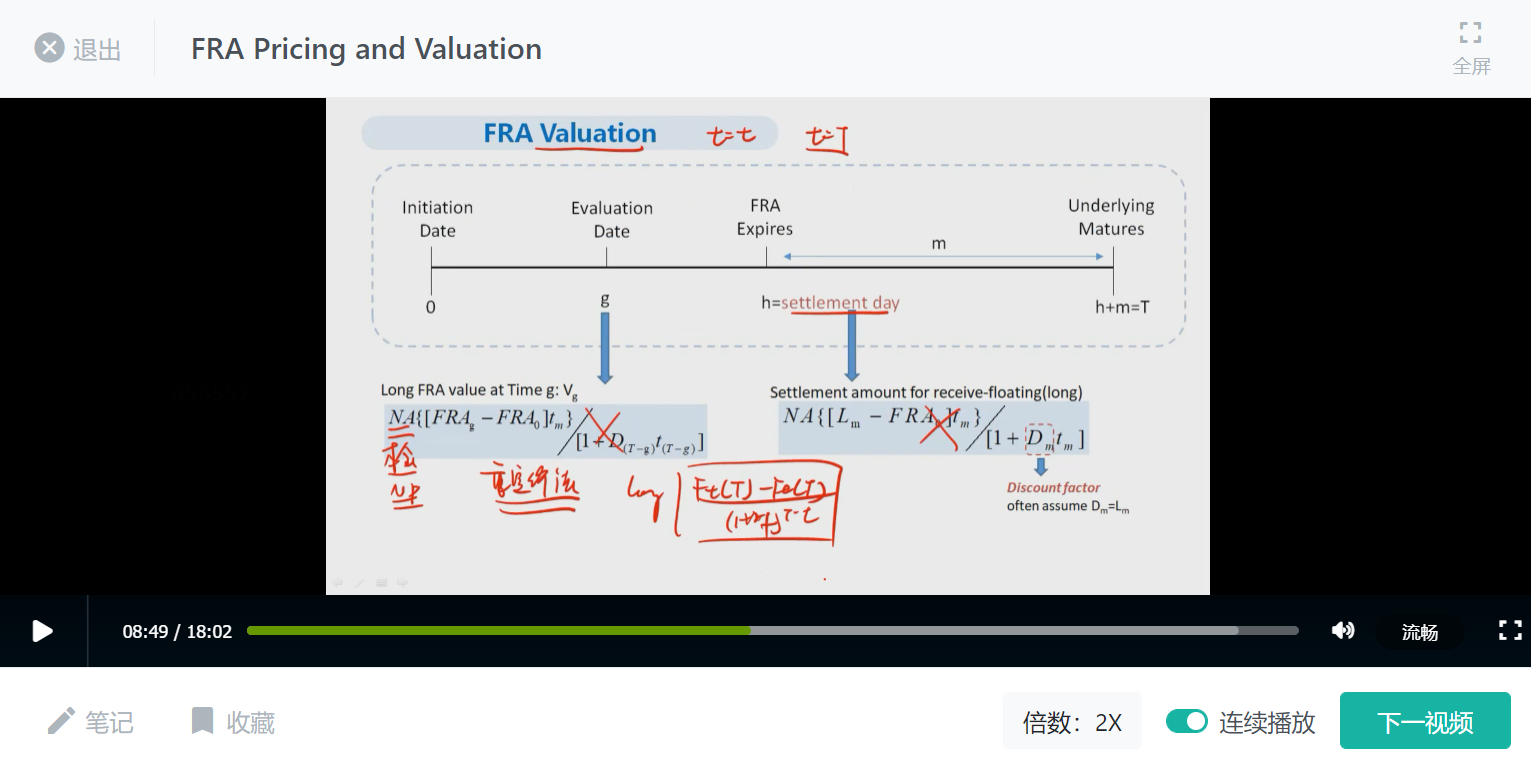

本题考察的是FRA的估值。上述方法使用的是重新定价法,还可以使用画图法,如下图:

老师能不能讲解一下重新定价法的解题过程,题目的解释没看懂,谢谢!