NO.PZ2019070101000012

问题如下:

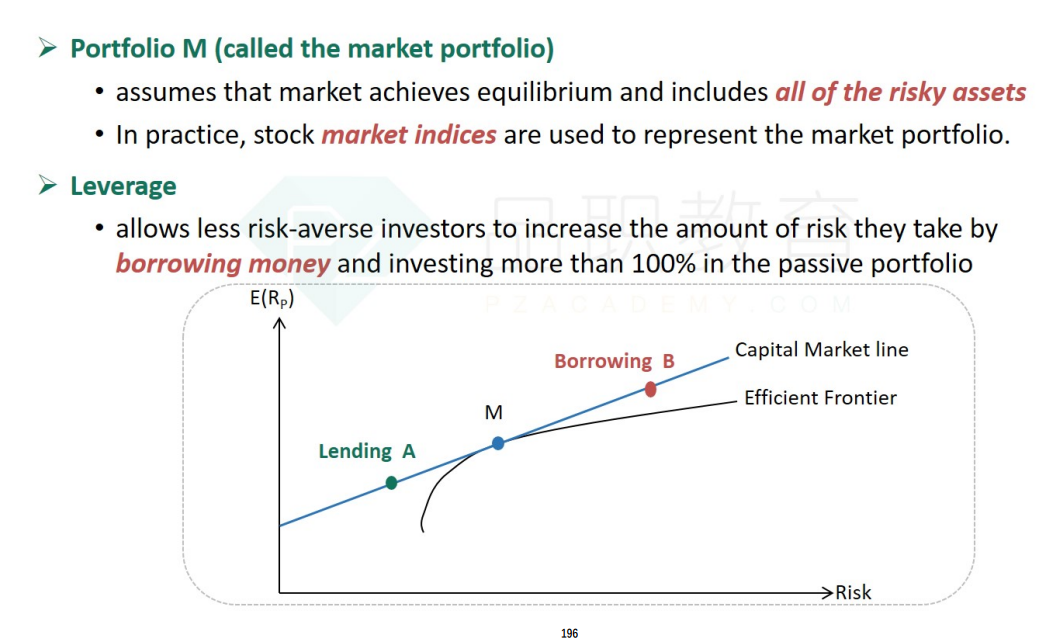

According to mean-variance model and taking the risk-free asset into consideration, to construct a portfolio for a risk-averse high-net wealth customer, it's appropriate to choose a portfilo:

选项:

A.on the efficient frontier.

B.below the efficient frontier.

C.on the asset allocation line and on the left side of the market portfolio.

D.on the asset allocation line and on the right side of the market portfolio.

解释:

C is correct.

考点:mean-variance model

解析:根据mean- variance model ,我们应该选择有限前沿上面的点进行投资,考虑无风险资产后,我们应该投资的点应该是在连接无风险资产与有效前沿切点的连线上,这个切点我们可以看成是市场组合。也就是在CAL上。由于这个客户是风险厌恶的客户,所以CAL上市场组合右边的点不适合它,因为这些点的投资需要使用杠杆。比较合适的就是选择CAL线上市场组合左边的点进行投资。C正确。

如题