NO.PZ2020021205000010

问题如下:

A stock price is currently 40. At the end of six months it will be either 36 or 44. The risk-free rate is 5% per annum with continuous compounding. What is the value of a six month European put option with a strike price of 40?

选项:

解释:

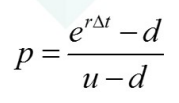

In this case, u = 44/40 = 1.1 and d = 36/40 = 0.9

so that:

p==0.6266

and the value of the option is

(0.6266 X 0 + 0.3734 x 4) x= 1.4568

老师这道题不是说either 44 or 36 那么每个结果不应该各占50%概率么