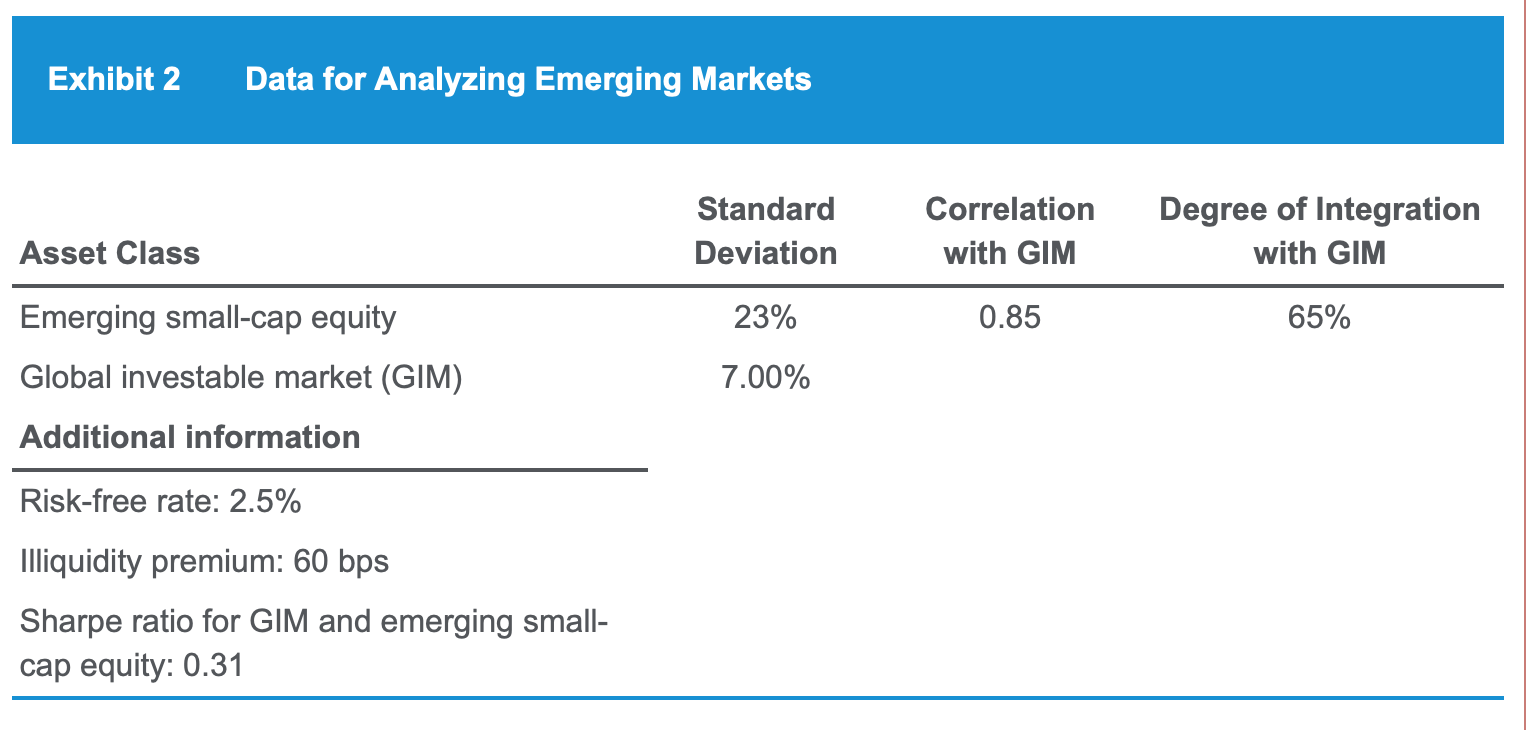

To assess the attractiveness of emerging market equities, Fiske suggests that they use the data in Exhibit 2 and determine the expected return of small-cap emerging market equities using the Singer–Terhaar approach.

Using the data in Exhibit 2 and Fiske’s suggested approach, the forecast of the expected return for small-cap emerging market equities is closest to:

- 8.9%.

- 9.9%.

- 9.5%.

答案:C is correct. The Singer and Terhaar approach for determining the expected return on an asset class involves determining the risk premium arising from systematic risk as a weighted average of the risk premiums arising from a fully integrated market and fully segmented market, where the weights for the fully integrated market is the degree of integration of the markets.

- The risk premium for the fully integrated market is given by:

- RPi = σiρi,M(RPM/σM) where (RPM/σM) is the Sharpe ratio for the world market portfolio

- The risk premium for the fully segmented market is given by: RPi = σi(RPM/σM)

- In addition, if there are market imperfections such as illiquidity premiums, they must be added in

- Finally, the expected return on the asset class is determined by adding these risk premiums to the risk-free rate, in the classical CAPM fashion.

Step 1Systematic risk premium in fully integrated market

Risk Premium: RPi = σiρi,M(RPM/σM)

= [23% × 0.85 × 0.31]

= 6.06%

Step 2Systematic risk premium in fully segmented market

Risk Premium: RPi = σi(RPM/σM)

= [23% × 0.31]

= 7.13%

Step 3Weight systematic risk premiums by degree of integration:

0.65 × 6.06 + 0.35 × 7.13 = 6.43%

Step 4Add the illiquidity premium

6.43% + 0.60% = 7.03%

Step 5Add the risk-free rate:

2.5% + 7.03% = 9.53%