NO.PZ2016031001000061

问题如下:

All three bonds are currently trading at par value.

Relative to Bond C, for a 200 basis point decrease in the required rate of return, Bond B will most likely exhibit a (n):

选项:

A.equal percentage price change.

B.greater percentage price change.

C.smaller percentage price change.

解释:

B is correct.

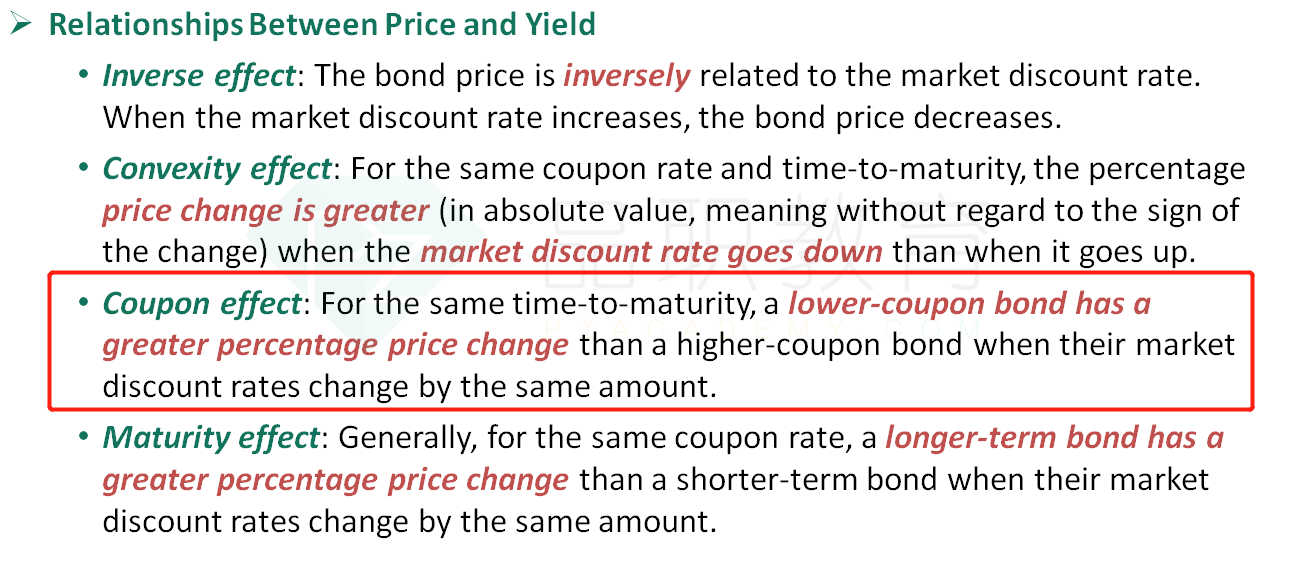

Generally, for two bonds with the same time-to-maturity, a lower coupon bond will experience a greater percentage price change than a higher coupon bond when their market discount rates change by the same amount. Bond B and Bond C have the same time-to-maturity (5 years); however, Bond B offers a lower coupon rate. Therefore, Bond B will likely experience a greater percentage change in price in comparison to Bond C.

考点:coupon effect

解析:coupon effect表明:对于maturity一样的债券,coupon rate较小的债券,其价格改变较大,也就是债券B相对于债券C,价格变化更大。故选项B正确。

发现视频里这一页没有讲,怎么理解Coupon rate下降,D上升?和P0有关系吗?