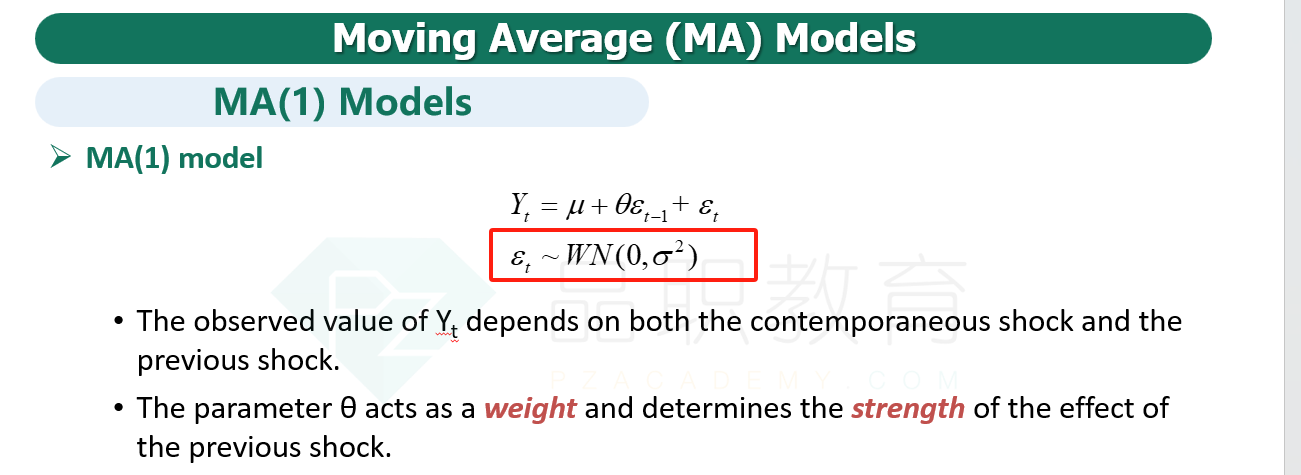

NO.PZ2019040801000057

问题如下:

There is a problem with the first-order moving average [MA(1)] process. Which of the following statements represents the problem and how to resolve it? The problem is the moving average representation of the MA(1) process:

选项:

A.incorporate only observable shocks, so the solution is to use a moving average representation.

B.incorporate unobservable shocks, so the solution is to use a moving average representation.

C.incorporate unobservable shocks, so the solution is to use an autoregressive representation.

D.incorporate only observable shocks, so the solution is to use an autoregressive representation.

解释:

C is correct.

考点:一阶移动平均

解析:一阶移动平均的问题在于它无法根据无法观察的白噪声冲击估计一个变量,解决方法是转换成自回归模型,使用可观察的项。

这道题的知识点是什么呢,是课上讲过的吗