Statement 1The most attractive feature of long–short equity managers is the lower beta sensitivity to equity markets than long-only equity managers.

Statement 2Dedicated short-bias managers typically benefit from higher levels of leverage and more frequent use of leverage than long–short or equity market neutral strategies.

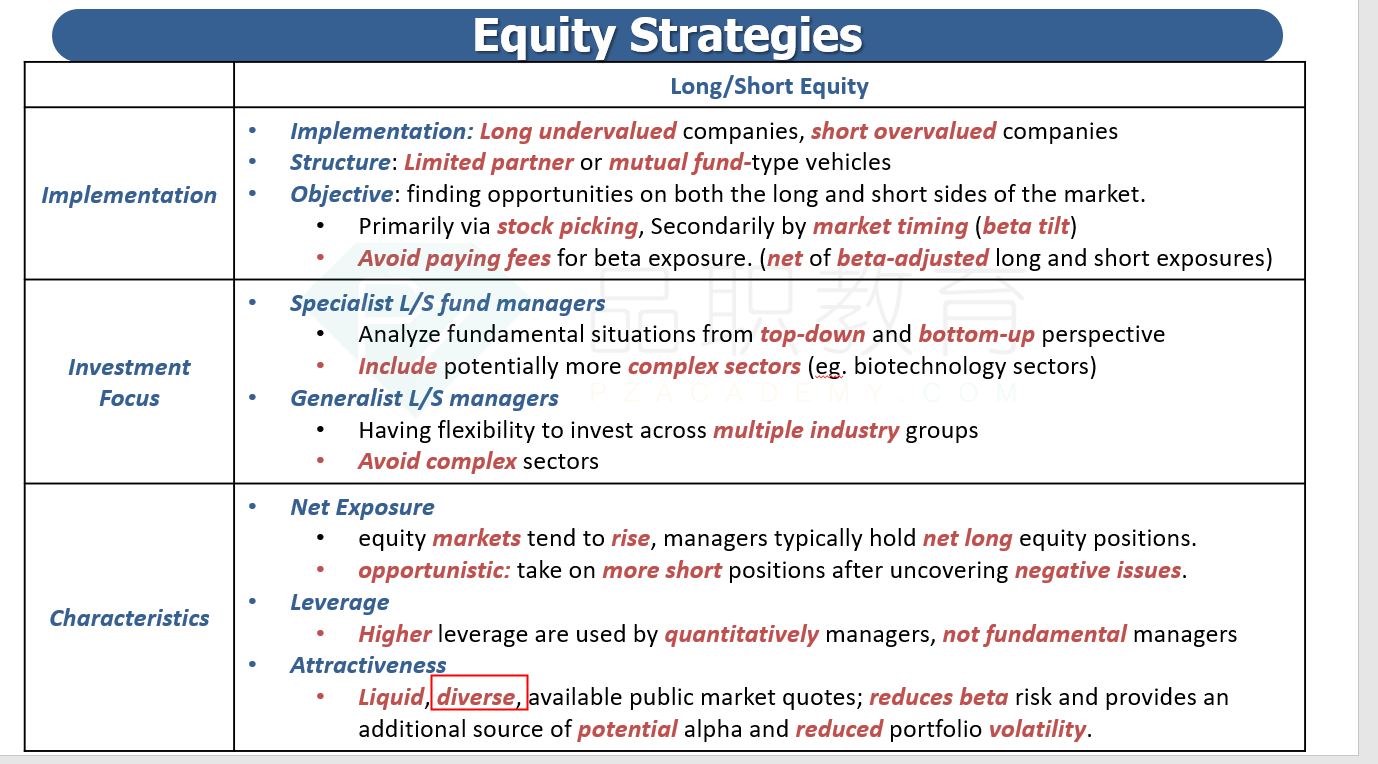

Statement 3Equity market–neutral managers are likely to have high levels of diversification and turnover ratios.

Which of Pukitis statement’s to Chu regarding equity-related hedge fund managers is most likely correct?

- Statement 1

- Statement 2

- Statement 3

Q'老师Long short 觉得并没有做到分散吧 long overvalue short undervalued