NO.PZ2020021204000049

问题如下:

Suppose that the six-month Libor rate is 5%, the forward Libor rate for the period between 0.5 and 1.0 year is 5.6% and the forward Libor rate for the period between 1.0 and 1.5 years is 6.0. The two-year Libor swap rate is 5.7%. All risk-free rates are 4.5%. What is the forward Libor rate for the period between 1.5 and 2.0 years? All rates are expressed with semi-annual compounding.

选项:

解释:

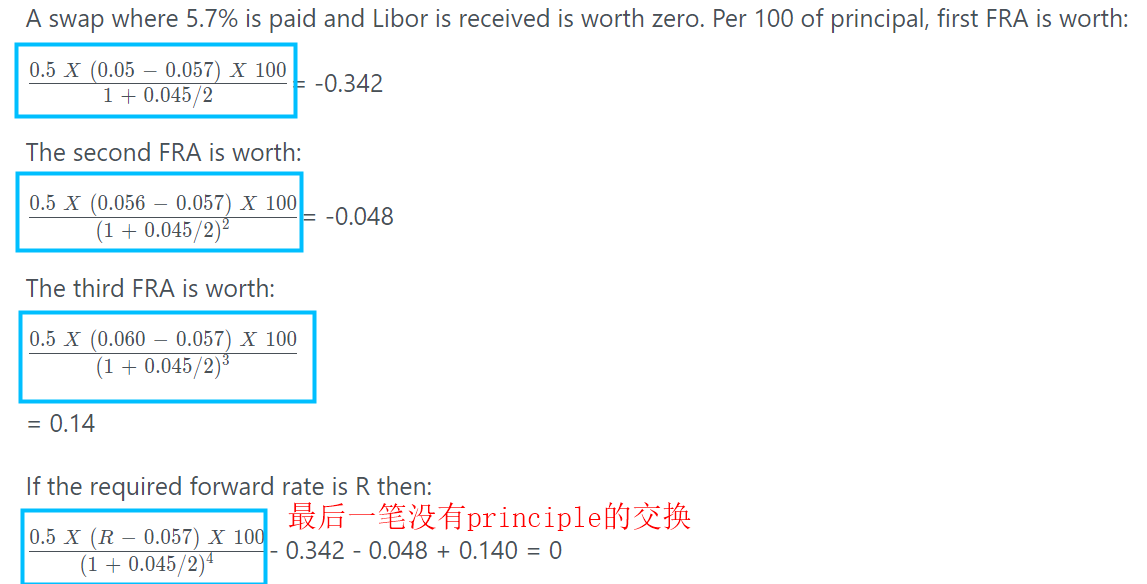

A swap where 5.7% is paid and Libor is received is worth zero. Per 100 of principal, first FRA is worth:

= -0.342

The second FRA is worth:

= -0.048

The third FRA is worth:

= 0.14

If the required forward rate is R then:

- 0.342 - 0.048 + 0.140 = 0

This can be solved to give R = 0.0625. The forward rate for the period between 1.5 and 2.0 years is 6.25% (semiannually compounded).

看了助教在别的问题下边的解释说:无所谓哪边收哪边付的,这题算的浮动端和固定端的PV是一致的就可以了,所以才有了最后的那个等式。等式的成立条件就是两个固定和浮动两端现金流相反且PV之和为0。FRA的思路是在swap签订的t=0时刻,value=0这个思路来计算的,这个swap在t=0.5,t=1,t=1.5 t=2.0四个时刻都会产生现金流支付的,所以fra的解法是围绕这个思路来进行的。可是如果按照bond的思维在0时刻浮动利率债券就回归面值NP了呀