NO.PZ2020021205000011

问题如下:

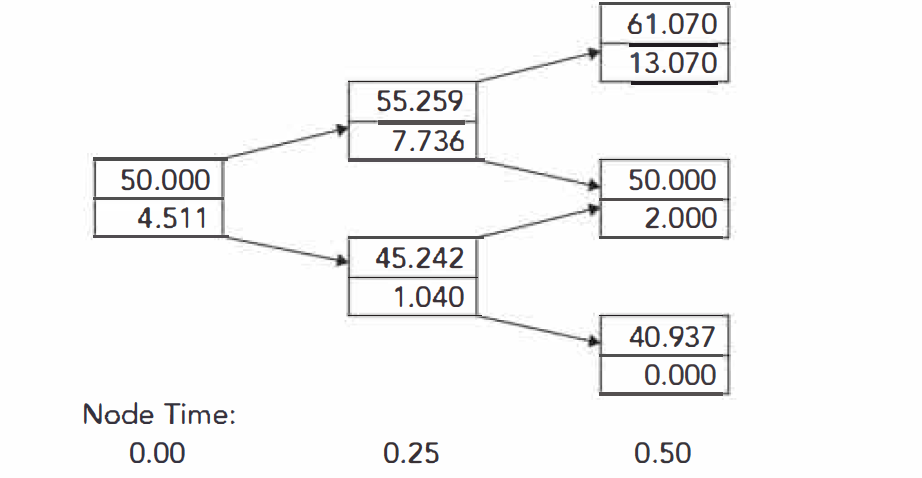

A stock price is currently 50. Its volatility is 20% per annum. The risk-free rate is 4% per annum with continuous compounding. Use a two-step tree to determine the value of a six-month European call option on the stock with a strike price of 48.

选项:

解释:

In this case, u = 1.1052, d = 0.9048, and p = 0.5252.

The following two-step tree shows that the value of the

option is 4.511.

- 为什么u=e^(10%*1)=0.1052 而不是u=e^(20%*sqrt(1/2))?

- p是怎么算出来的?用公式e^(r^change in t)-d/(u-d)里r和change in t分别是多少?为什么?