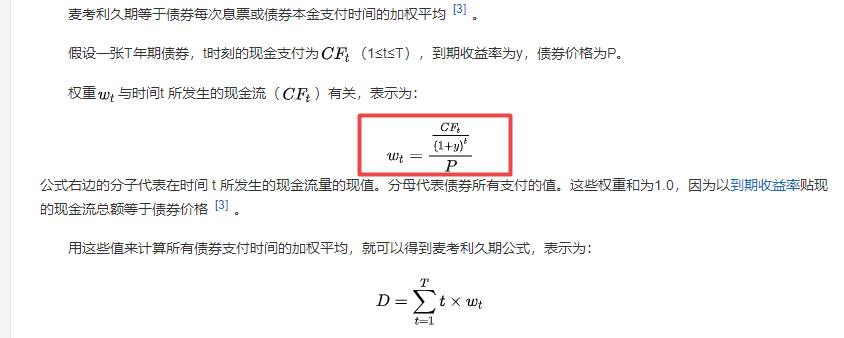

No.PZ2020021204000018 (问答题)

来源: 原版书

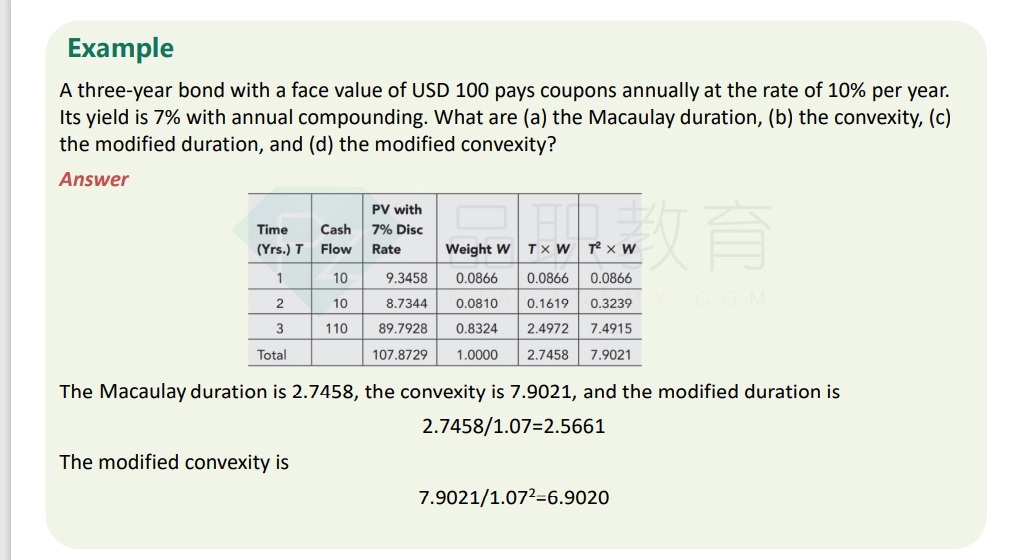

A three-year bond with a face value of USD 100 pays coupons annually at the rate of 10% per year. Its yield is 7% with annual compounding. What are (a) the Macaulay duration, (b) the convexity, (c) the modified duration, and (d) the modified convexity?

可以麻烦老师给出macaulay久期和凸性的计算过程吗