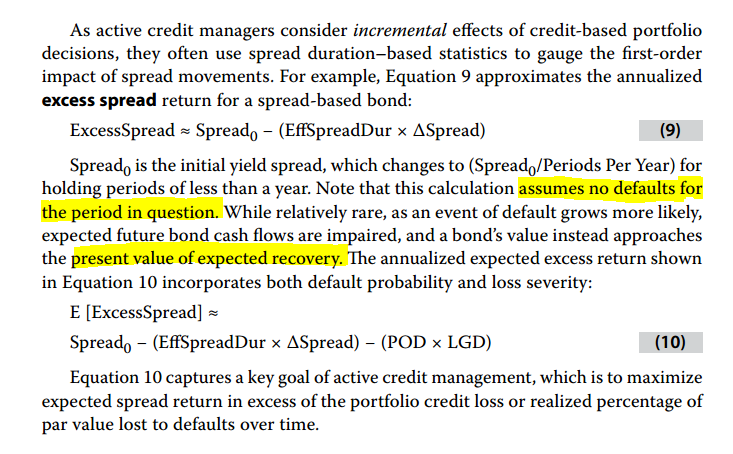

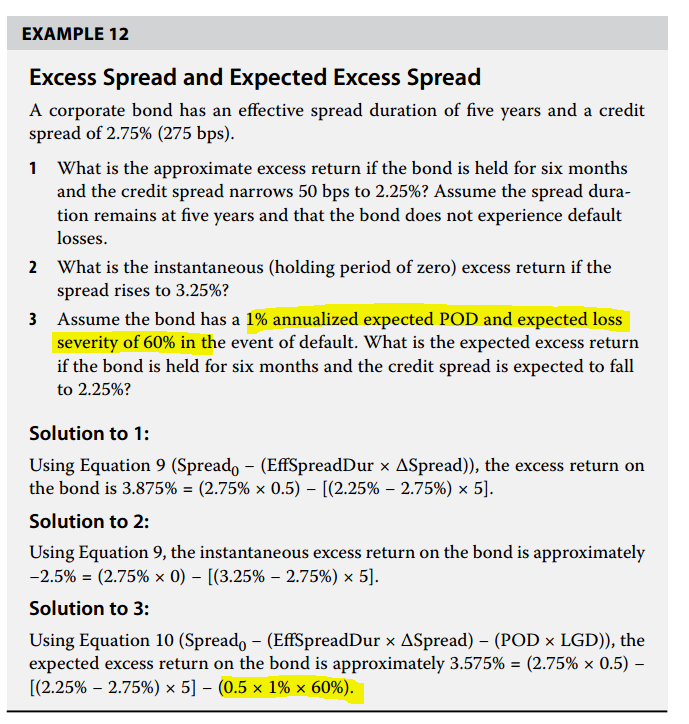

在视频讲义里,老师说之所以要加上expected loss是因为这个公式里面的loss是expected,而题目里所说的 assuming no default loss是指current,所以我们要加这个expected loss。但是在我之前提问的过程中,辅导员说因为题目中说assume no default,所以不应该加这个expected loss。我现在对于要不要加特别困惑

我回去翻了一下原版书,P82的定义是“Note that this calculation (9) assumes no defaults for the period in question. ”但是P83的例题里用的是expected POD和loss severity算的。所以在这个excess spread return里,到底应该不应该含expected POD * Loss Severity