NO.PZ2016062402000052

问题如下:

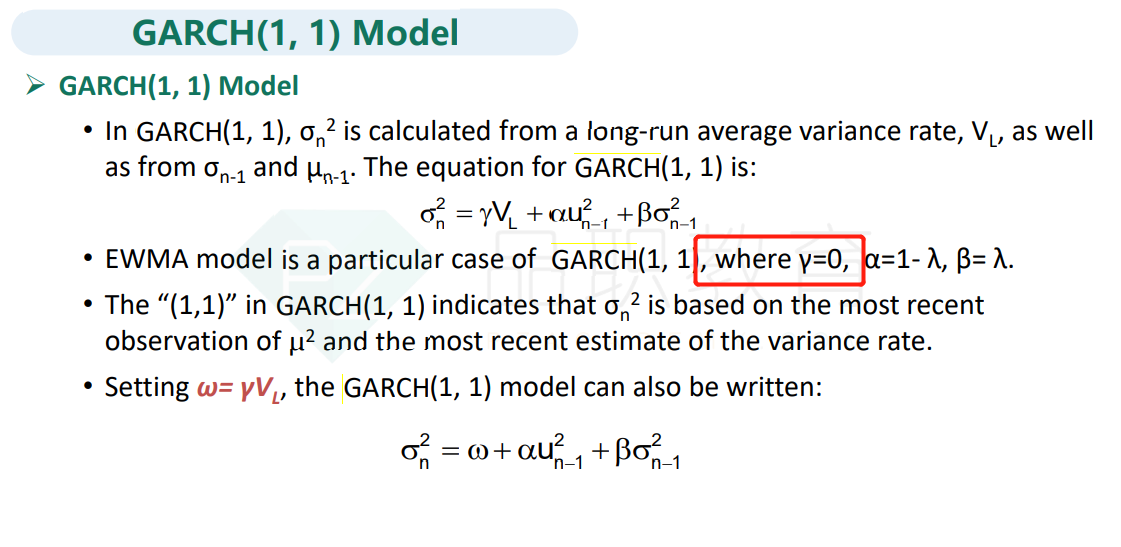

Which of the following four statements on models for estimating volatility is incorrect ?

选项: In

the EWMA model, some positive weight is assigned to the long-run average

variance rate.

In the EWMA model, the weights assigned to observations decrease exponentially as the observations become older.

C.In the GARCH(1,1) model, a positive weight is estimated for the long- run average variance rate.

D.In the GARCH(1,1) model, the weights estimated for observations decrease exponentially as the observations become older.

解释:

The GARCH model has a finite unconditional variance, so statement c. is correct. In contrast, because sum to 1, the EWMA model has undefined long-run average variance. In both models weights decline exponentially with time.

在EWMA模型中,长期平均方差的权重不是r吗?为什么说权重为0?