NO.PZ2019122802000023

问题如下:

John Puten is the chief investment officer of the Markus University Endowment Investment Office. Puten seeks to increase the diversification

of the endowment by investing in hedge funds. He recently met with

several hedge fund managers that employ different investment strategies.

In selecting a hedge fund manager, Puten prefers to hire a manager that

uses the following:

● Fundamental and technical analysis to value markets

● Discretionary and systematic modes of implementation

● Top-down strategies

●

A range of macroeconomic and fundamental models to express a view

regarding the direction or relative value of a particular asset

Puten’s staff prepares a brief summary of two potential hedge fund investments:

Hedge Fund 1: A relative value strategy fund focusing only on convertible arbitrage.

Hedge Fund 2: An opportunistic strategy fund focusing only on global macro strategies.

Determine which hedge fund would be most appropriate for Puten. Justify your response.

选项:

解释:

Hedge Fund 2 would be most appropriate for Puten because it follows a global macro strategy, which is consistent with Puten’s preferences.

Global macro managers use both fundamental and technical analysis to

value markets, and they use discretionary and systematic modes of

implementation. The key source of returns in global macro strategies

revolves around correctly discerning and capitalizing on trends in

global markets.

Global macro strategies are typically top-down and

employ a range of macroeconomic and fundamental models to express a view

regarding the direction or relative value of a particular asset or

asset class. Positions may comprise a mix of individual securities,

baskets of securities, index futures, foreign exchange futures/forwards,

fixed-income products or futures, and derivatives or options on any of

the above. If the hedge fund manager is making a directional bet, then

directional models will use fundamental data regarding a specific market

or asset to determine if it is undervalued or overvalued relative to

history and the expected macro-trend.

Hedge Fund 1 follows a relative

value strategy with a focus on convertible arbitrage, which is not

aligned with Puten’s preferences. In a convertible bond arbitrage

strategy, the manager strives to extract “cheap” implied volatility by

buying the relatively undervalued convertible bond and taking a short

position in the relatively overvalued common stock. Convertible

arbitrage managers are typically neither using fundamental and technical

analysis to value markets nor employing top-down strategies to express a

view regarding the direction or relative value of an asset.

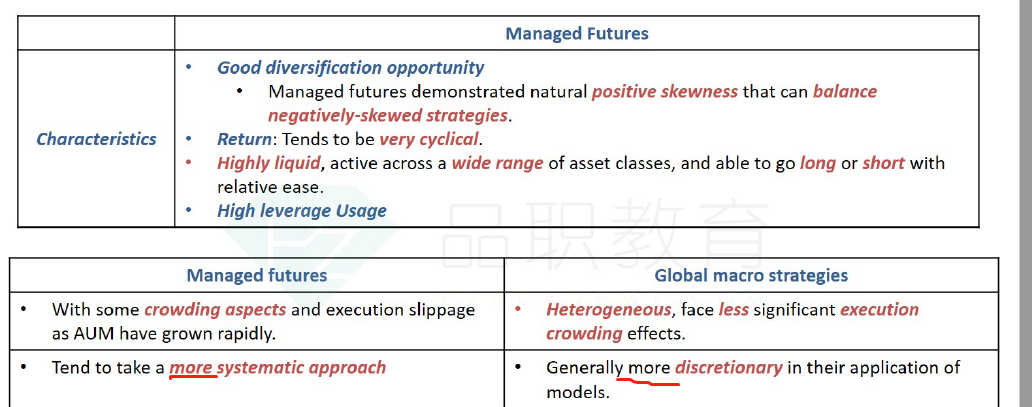

这个题同学可能会纠结,题目中要求systematic和discretionary。但是误以为Global macro只有discretionary呀,而实际global macro是‘主要’用discretionary”,什么是主要,就是大部分,那还有一部分就不是对吧。参看框架图的讲义,这里说的是more,也就是相对来说。并不是绝对的。做这个题我们把握大方向就好。

可以总结一个简写的答案吗?