NO.PZ201601050100000302

问题如下:

2. For Subscriber 2, and assuming all of the choices relate to the KRW/USD exchange rate, the best way to implement the trading strategy would be to:

选项:

A.write a straddle.

B.buy a put option.

C.use a long NDF position.

解释:

C is correct.

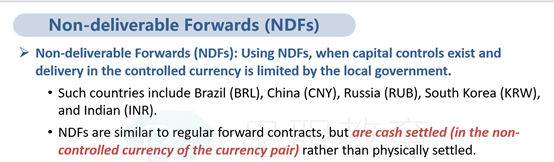

Based on predicted export trends, Subscriber 2 most likely expects the KRW/USD rate to appreciate (i.e., the won—the price currency—to depreciate relative to the USD). This would require a long forward position in a forward contract, but as a country with capital controls, a NDF would be used instead. (Note: While forward contracts offered by banks are generally an institutional product, not retail, the retail version of a non-deliverable forward contract is known as a -contract for differences- (CFD) and is available at several retail FX brokers.)

A is incorrect because Subscriber 2 expects the KRW/USD rate to appreciate. A short straddle position would be used when the direction of exchange rate movement is unknown and volatility is expected to remain low.

B is incorrect because a put option would profit from a depreciation of the KRW/USD rate, not an appreciation (as expected). Higher volatility would also make buying a put option more expensive.

中文解析:

本小题讨论的是Subscriber 2(2号订阅者),对应题干信息说到:韩国出口下降而美国出口上升(“United states is experiencing a rise in exports”),一国的出口增加将会使得本币升值,因此美元将会升值。可以这样理解,美国的出口增加,那么市场上需要更多地美元来购买这些商品,对美元的需求增加,美元就升值了。

关于选项:

因为题干中说到预测波动率会增加,因此不应该write a straddle,因为这是赌波动率会不变或者下降的,A错。

标价形式为KRW/USD,我们研究的是USD,而USD升值,所以不应buy a put option. B错。

预测USD会升值,我们需要做USD升值可以获利的头寸,因此long forward,又因为资本管制的原因,所以我们选择使用NDF。C对

老师,想问三个问题,谢谢。

- 为什么美国出口增加,美元是升值???难道不是美元贬值,更便宜,出口才会增加啊,因为卖的便宜,其他人才愿意买.

- 什么是NDF?

- 如果判断美元会升值,那么有利的策略就是long forward on USD(提前锁定美元汇率)?