NO.PZ2019052801000068

问题如下:

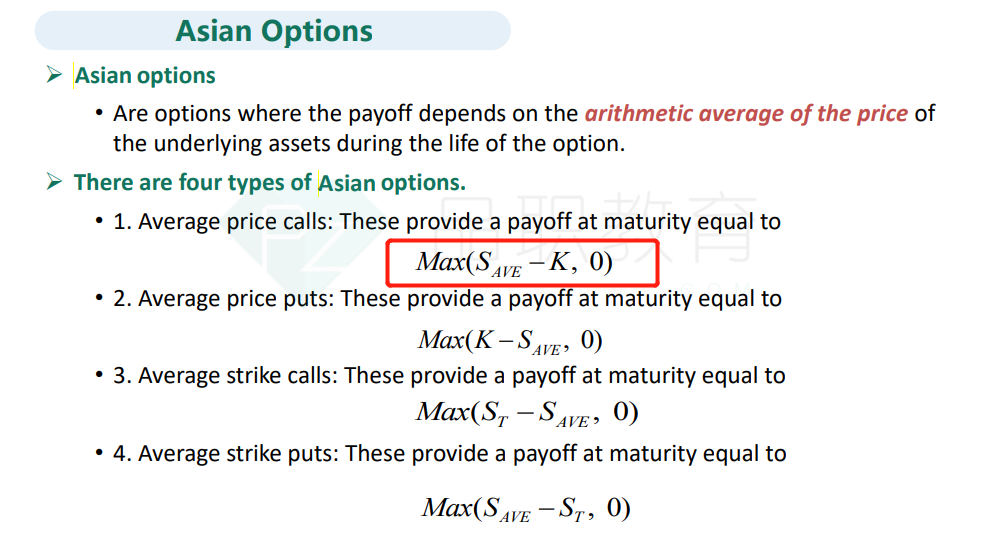

Which of the following statement is most appropriate regarding Asian option?

选项:

A.The payoff depends on the arithmetic average of the underlying asset prices during the option life.

B.The payoff depends on the maximum or minimum asset price reached during the option life.

C.The payoff from Asian call option is the maximum of strike price minus the average price of the underlying asset and zero.

D.The payoff from Asian call option is the maximum of the maximum price of the underlying asset minus strike price and zero.

解释:

A is correct.

考点:Asian option

解析:Asian option是通过标的物特定期间的平均价格而决定回报的期权,A选项正确。Asian call option的收入可以这样计算:c=Max(SAVE-K,0)。

B和D选项说的是Lookback option的定义以及收入计算方式。

请问这题C为什么不对?