NO.PZ2020021203000120

问题如下:

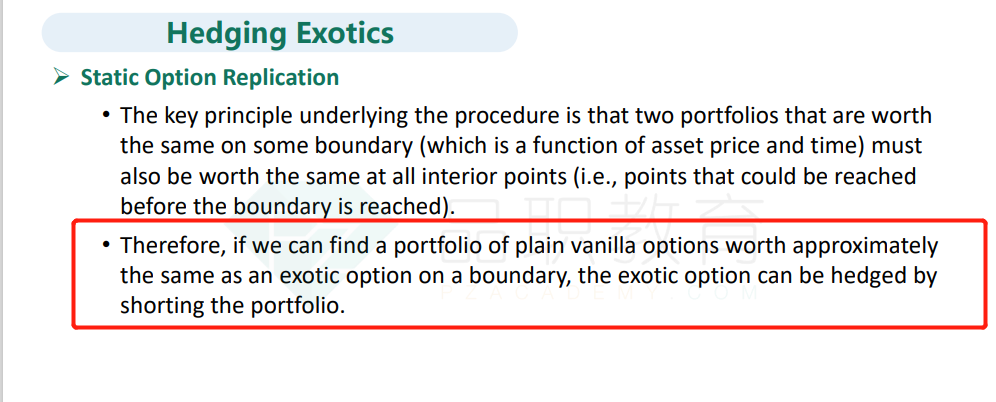

What is the key theoretical result underlying static options replication?

解释:

If two portfolios have the same value on some boundary in {S, t} space they must have the same value at interior points (i.e., all points that could be reached prior to the boundary being reached).

麻烦老师翻译一下,谢谢