这道题能延伸说明一下么,谢谢

No.PZ2021050702000006 (选择题)

来源:

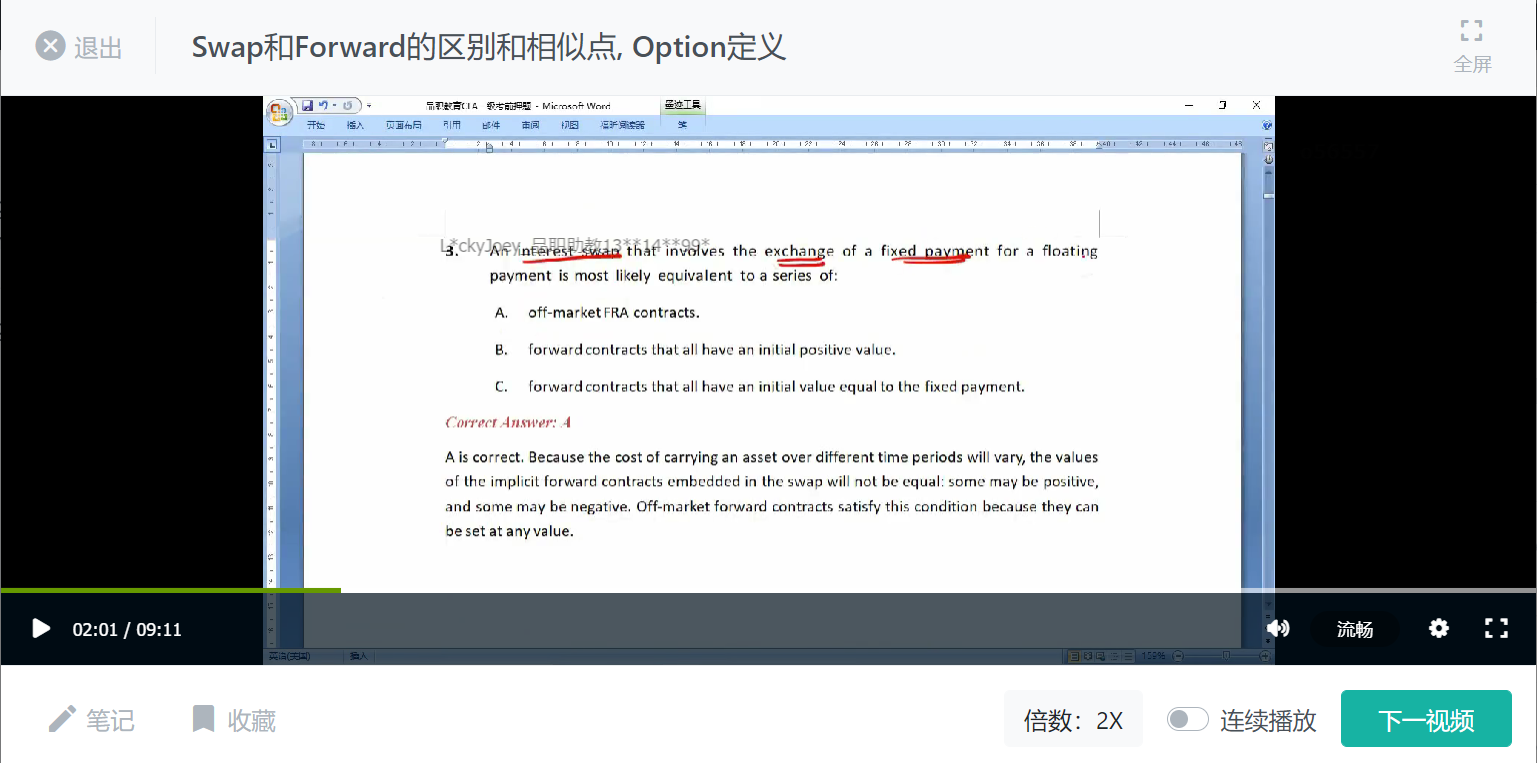

An interest swap that involves the exchange of a fixed payment for a floating payment is most likely equivalent to a series of:

您的回答C, 正确答案是: A

A

off-market FRA contracts.

B

forward contracts that all have an initial positive value.

C

不正确forward contracts that all have an initial value equal to the fixed payment.

Correct Answer: A

A is correct. Because the cost of carrying an asset over different time periods will vary, the values of the implicit forward contracts embedded in the swap will not be equal: some may be positive, and some may be negative. Off-market forward contracts satisfy this condition because they can be set at any value.

考点:衍生-Derivative Markets and Instruments- Swap和Forward的区别和相似点