NO.PZ2018091706000043

问题如下:

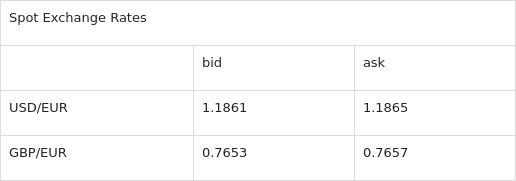

BBQ firm is an British company and exports steel to a firm which is in USA. Assume BBQ receives the payment of $3,600,000 . BBQ observes the spot exchange rates as the following table shows:

Then he calls a dealer who quotes 1.5500 USD/GBP for bid and 1.5505 for ask. According to the above information BBQ enters a triangular arbitrage transaction. The profit on USD 3,600,000 payment is closest to

选项:

A. 0.

B. USD 6,300.

C. GBP 6,300.

解释:

A is correct.

考点:Triangular arbitrage

解析:首先我们根据题干表格的第三、第四行,通过交叉汇率求解得关于USD/GBP的市场报价。

由此我们知道,相对于DealerA的报价( 1.5500-15505 ),市场 对于GBP的报价便宜( 1.5490-1.5504 )。但是这里依然没有套利空间的存在。因为,虽然BBQ可以从市场以1.5504USD/GBP的价格买入GBP,但是他没有办法以高于1.5500USD/GBP的价格把GBP卖给DelaerA。那么货币的买入价1.5504大于卖出价1.5500,所以不存在套利空间。套利利润为0.

我理解了本题做法。但想请老师列出整个货币转换过程:USD3,600,000—EUR(1.1861/1.1865 USD/EUR)—GBP(0.7653/0.7657 GBP/EUR)—USD(1.5500/1.5505USD/GBP),我不是很确定每一步哪个用BID PRICE哪个用ASK PRICE。 谢谢!