No.PZ2021051201000013 (选择题)

来源:

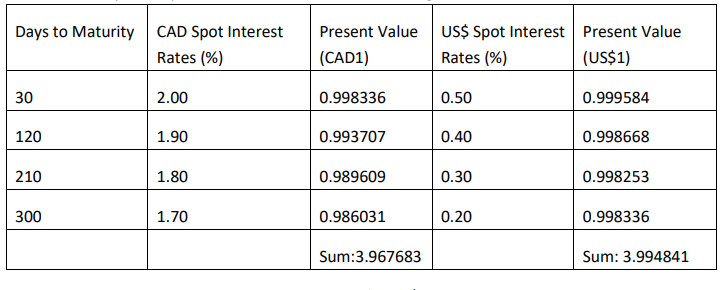

A US company needed to borrow 100 million Canadian dollars (CAD) for one year for its Canadian subsidiary. The company decided to borrow in US dollars (US$) an amount equivalent to CAD 100 million by issuing US-denominated bonds. The company entered into a one-year currency swap with a swap dealer. The swap uses quarterly reset (30/360 day count) and exchange of notional amounts at initiation and at maturity. At the swap’s expiration, the US company pays the notional amount in Canadian dollars and receives from the dealer the notional amount in US dollars. The fixed rates were 2.7695% for Canadian dollars and 0.2497% for US dollars. Initially, the notional amount in US dollars was US$87,719,298 with a spot exchange rate of CAD1.14 for US$1.

Assume 60 days have passed and we observe the following market information:

The currency spot exchange rate is now CAD1.13 for US$1.

The current value to the swap dealer in CAD of the currency swap entered into 60 days ago will be closest to:

您的回答A, 正确答案是: C

A

不正确–CAD13,557,000.

B

CAD637,620.

C

CAD2,145,200.

数据统计(全部)

做对次数: 85

做错次数: 218

正确率: 28.05%

数据统计(个人)

做对次数: 0

做错次数: 0

正确率: 0%

解析

Correct Answer: C

考点:衍生- Pricing and Valuation of Forward Commitment – Pricing and Valuation of Currency Swap