NO.PZ202108100100000406

问题如下:

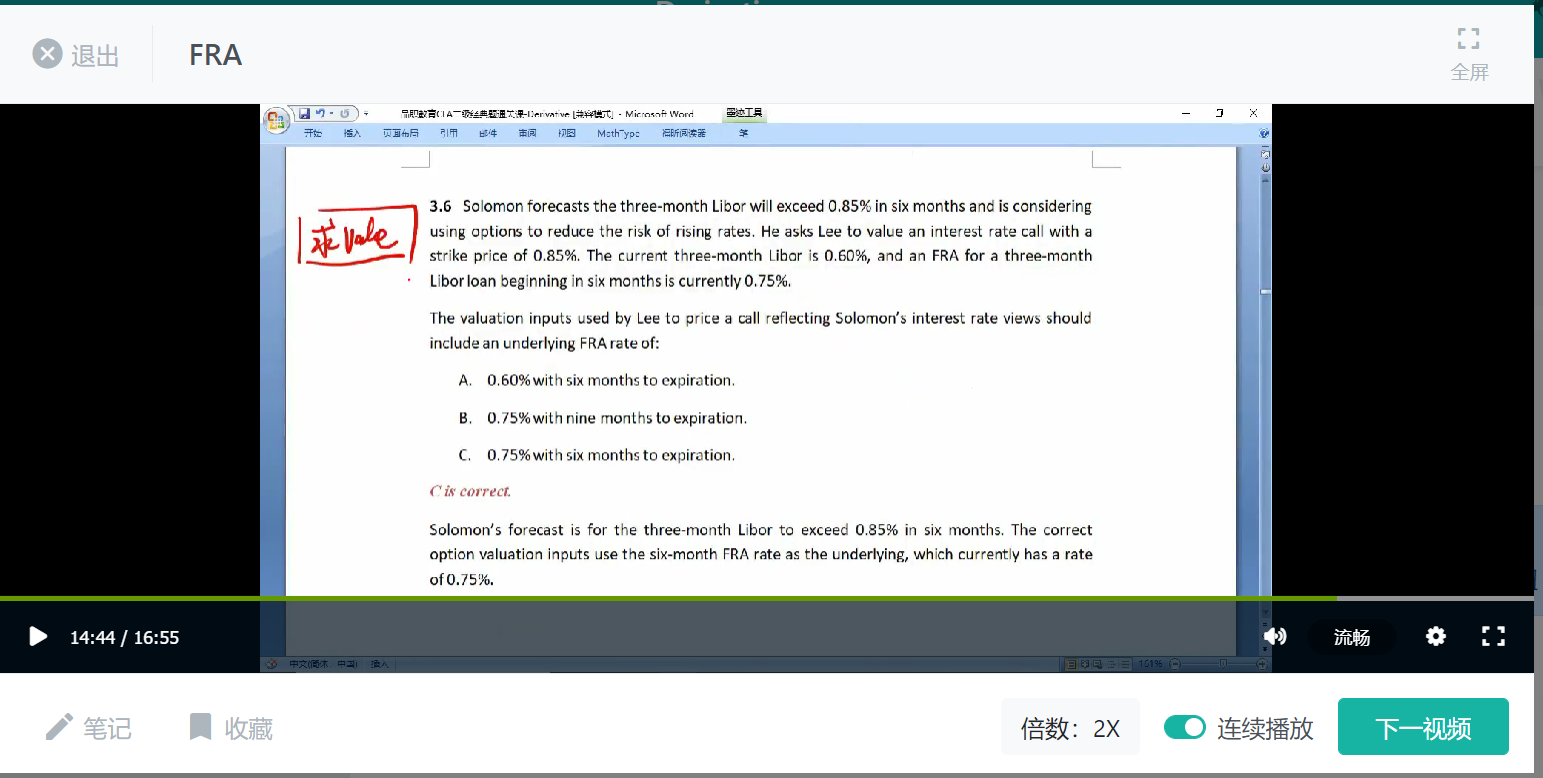

The valuation inputs used by Lee to price a call reflecting Solomon’s interest

rate views should include an underlying FRA rate of:

选项:

A.0.60% with six months to expiration.

0.75% with nine months to expiration.

0.75% with six months to expiration.

解释:

C is correct.

Solomon’s forecast is for the three-month Libor to exceed 0.85% in six months. The correct option valuation inputs use the six-month FRA rate as the underlying, which currently has a rate of 0.75%.

中文解析:

该利率期权的标的注意是FRA即0.75%。根据题干信息可知,这是一个6×9的FRA,因此FRA是在6个月的时候到期,FRA结束后开始的loan是在9个月到期,因此本题选C。

您好这个FRA的6*9请问能否画个图标一下,我感觉自己有点懵,想知道0.6等题目里的各类利率的在时间线上标注