NO.PZ2021120102000021

问题如下:

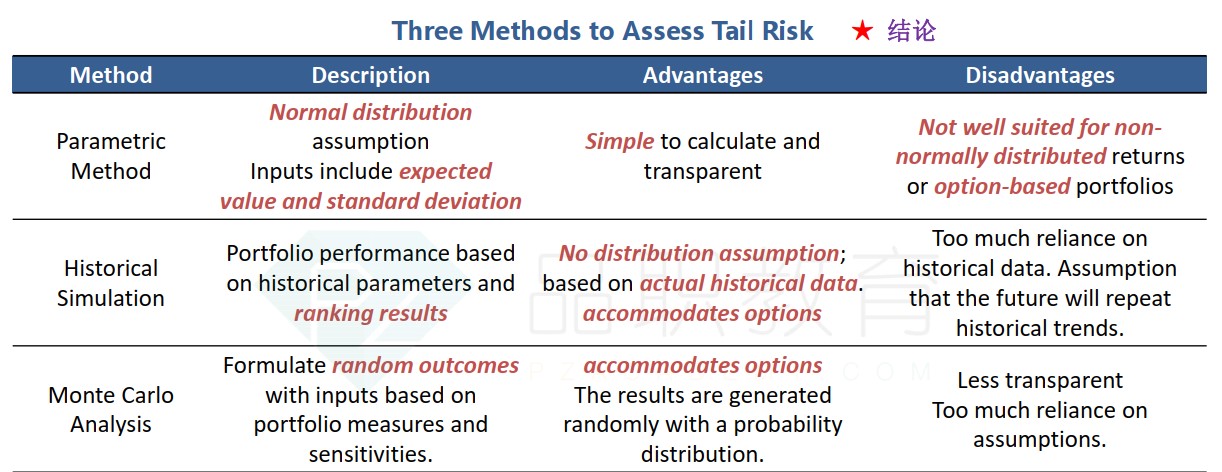

Which of the following statements best describes methods for assessing portfolio tail risk?

选项:

A.

Parametric methods use expected value and standard deviation of

risk factors under a normal distribution and are well suited for option-based portfolios.

B.

Historical simulation methods use historical parameters and ranking results and are not well suited for option-based portfolios.

C.

Monte Carlo methods generate random outcomes using portfolio measures and sensitivities and are well suited for option-based portfolios.

解释:

C is correct. Parametric methods in A are not well suited for non-normally distributed returns or option-based portfolios, while historical simulation assumes no probability distribution and accommodates options.

同题目 B选项哪里错了