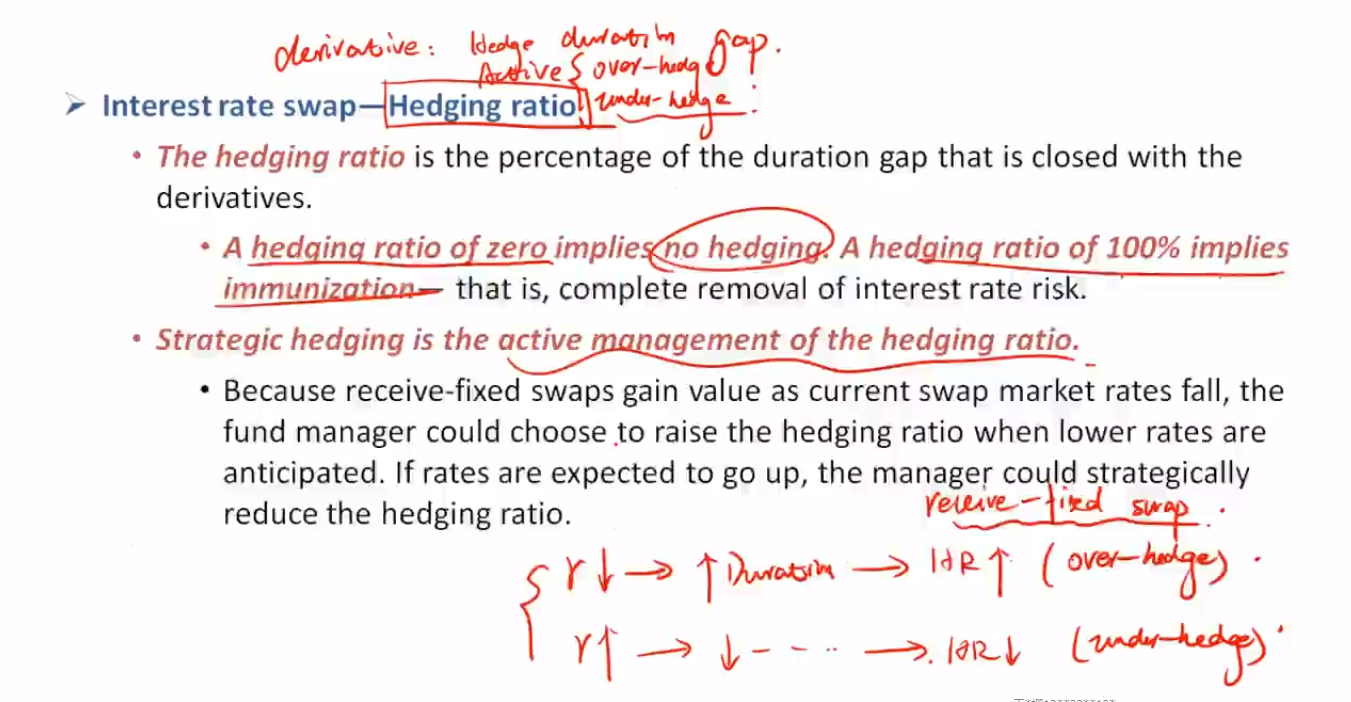

老师基础课上讲:只要实际比fully hedge的衍生品份数多就是overhedge,不管它是long还是short。 那同理,只要实际比fully hedge的衍生品份数少就是underhedge,不管它是long还是short。

但是,基础课的这里又说了另一个逻辑,即让duration增加就是overhedge; 减少duration就是underhedge。

前后矛盾啊.....

pzqa015 · 2022年01月27日

嗨,爱思考的PZer你好:

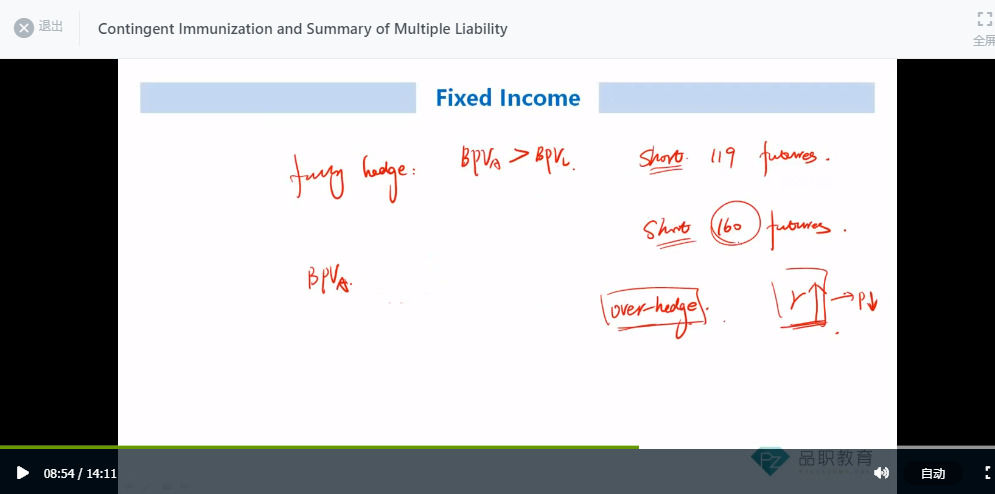

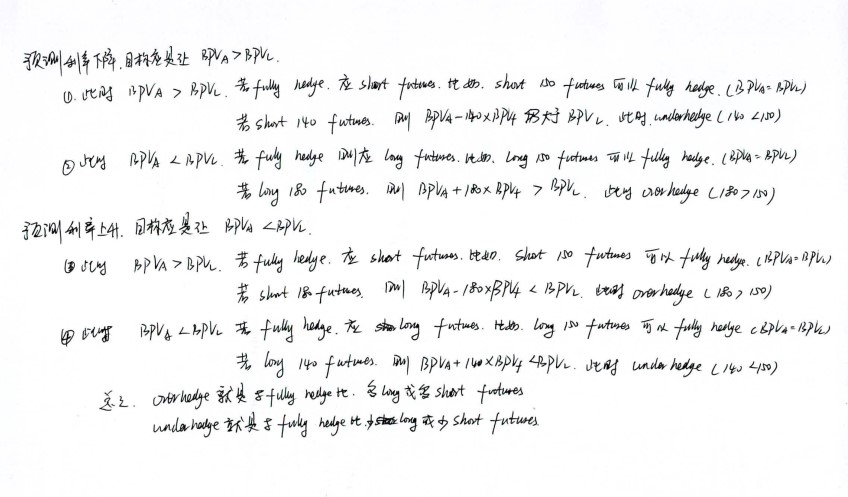

这里的总结见这个图片了。

不是说让duration增加就是overhedge; 减少duration就是underhedge。

而是如果预期利率下降,那么增加duration并超过liability的duration,是overhedge,反之没超过,是underhedge。

如果预期利率下降,那么降低duration并超过liability的duration,是overhedge,反之没超过,是underhedge。

----------------------------------------------努力的时光都是限量版,加油!

tujinjin · 2022年01月28日

好全面的总结 我理解了 就是让BPV变号的:>变< or <变>都是overhedge; ><号没变的就是underhedge