NO.PZ2018070201000108

问题如下:

If the portfolio is not fully diversified, which of the following is most suitable permormance measures?

选项:

A. M-squared.

B. Treynor ratio.

C. Jensen’s alpha.

解释:

A is the correct.

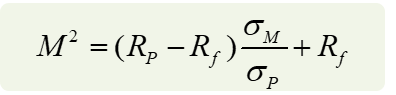

When a portfolio is not fully diversified, the appropriate performance measures should be M-squared which is based on total risk.

不能被完全分散,说明有系统性风险,为什么用total risk;或者能否再解釋下題目呢,謝謝