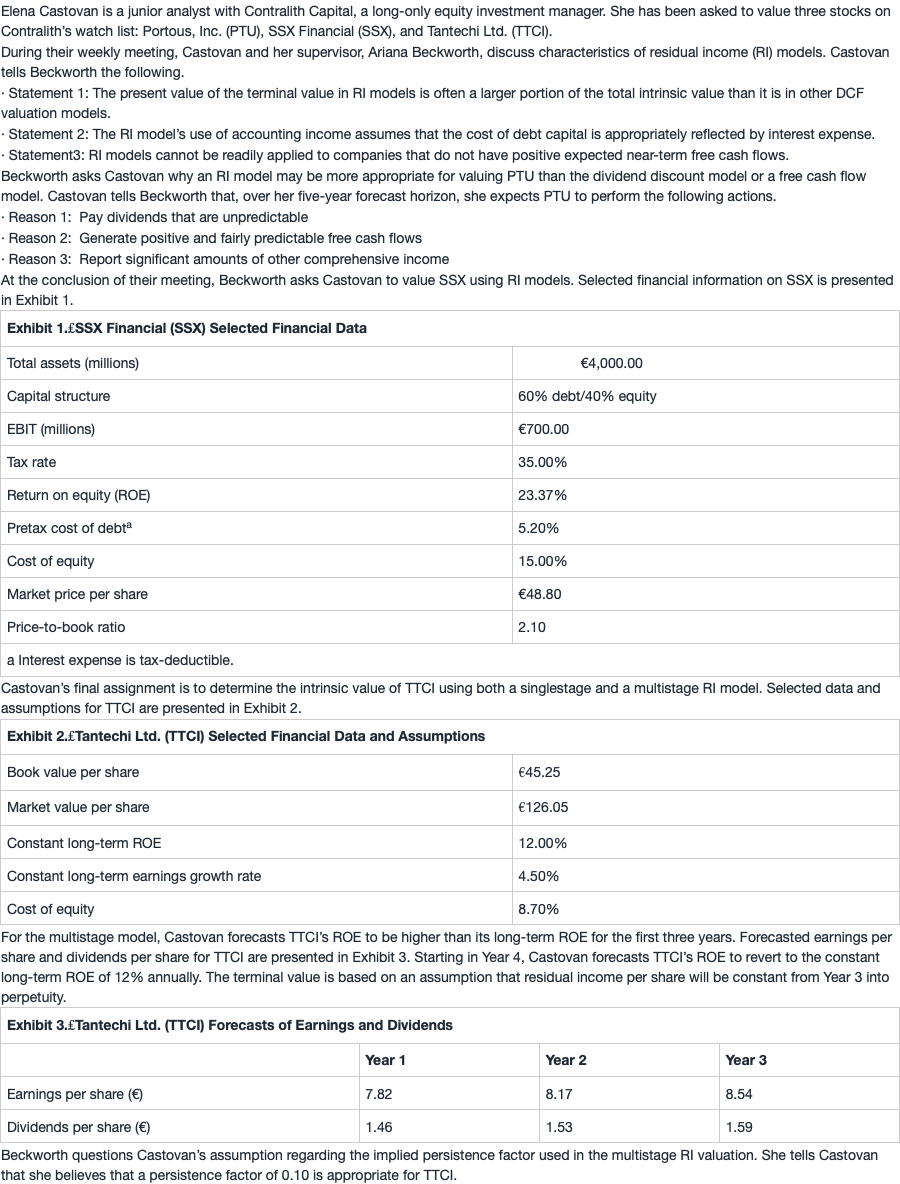

NO.PZ201710200100000408

问题如下:

8. Based on Exhibits 2 and 3 and the multistage RI model, Castovan should estimate the intrinsic value of TTCI to be closest to:

选项:

A.€54.88.

B.€83.01.

C.€85.71.

解释:

C is correct.

Residual income per share for the next three years is calculated as follows.

Because Castovan forecasts that residual income per share will be constant into perpetuity, equal to Year 3 residual income per share, the present value of the terminal value is calculated using a persistence factor of 1.

Present value of terminal value =

= =33.78

So, the intrinsic value of TTCI is then calculated as follows.

V0==85.71

不是应该计算PVri3么

韩韩_品职助教 · 5 个月前

嗨,爱思考的PZer你好:

同学你好:

答案的公式显示有点问题,本来是全部合并在一起了,我们分开来写一下,我们这是一个两阶段的RI估值模型,第一阶段是前2年,前2年的RI计算上,答案的表格中已经展示的很清楚了,我们就直接采用了:RI1=3.88,RI2=3.68;而从第三年开始,RI3=3.47,恒定了,w=1,所以根据公式:PVRI3=(RI*w)/(1+r-w)=3.47*1/(1+0.087-1)=39.89,但记住,这是第二年末这个时间点的终值,到时候还要在折现到估值的0时刻。

现在根据股指公式V=B0+PVRI1+PVRI2+PVTV=45.25+3.88/(1+8.7%)+3.68/(1+8.7%)^2+39.89/(1+8.7%)^2=85.7

关键是画图,找好两阶段的分界点,看到底折到哪一时刻;

1.为什么 求V的时候 RI3不用在折现了?

2.老师能不能画图 看看我错在哪里?