NO.PZ2021062201000011

问题如下:

A portfolio has an expected mean return of 8% and standard deviation of 14%. The probability that its return falls between 8% and 11% is closest to:

选项:

A. 8.5%

B. 14.8%

C. 58.3%

解释:

A is correct.

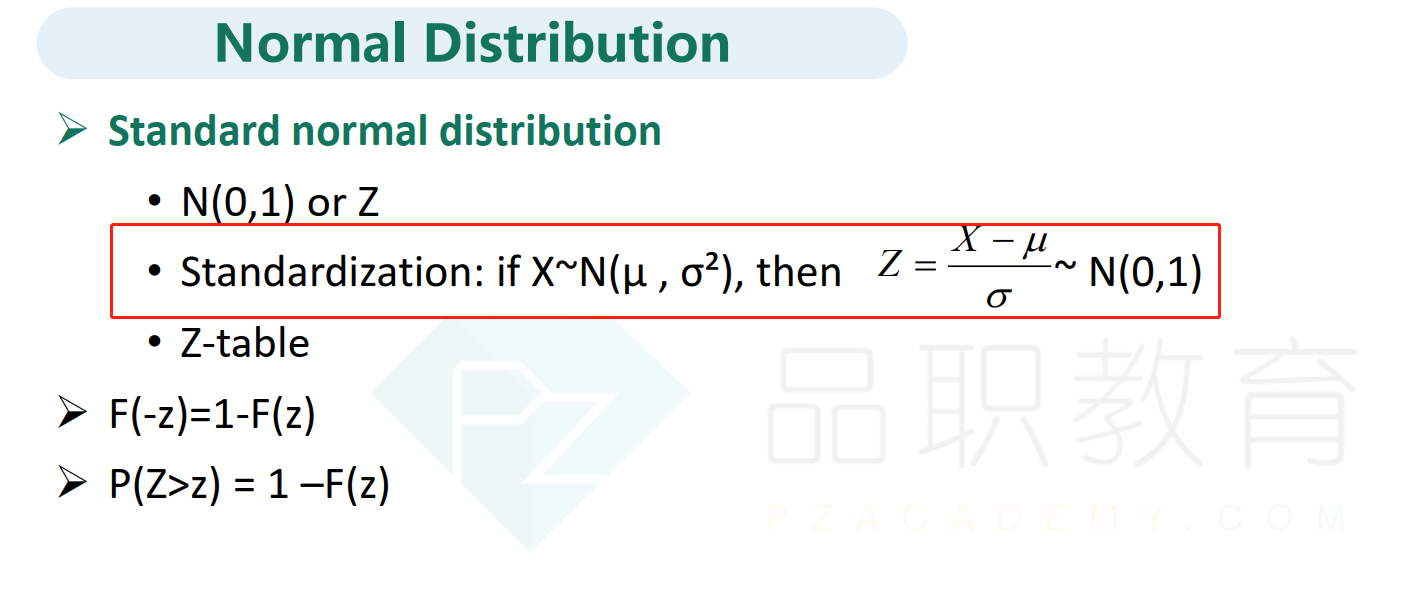

P(8%

≤ Portfolio return ≤ 11%) = N(Z corresponding to 11%) – N(Z corresponding

to 8%).

For the first

term, NORM.S.DIST(11% – 8%)/14% = 58.48%. To get the second term

immediately, note that 8% is the mean, and for the normal distribution, 50% of

the probability lies on either side of the mean.

Therefore, N(Z corresponding to 8%) must equal 50%, So, P(8% ≤

Portfolio return ≤ 11%) = 0.5848 - 0.50 = 0.0848, or approximately 8.5%.

基于下列总公式:

P(8% ≤ Portfolio return ≤ 11%) = N(Z corresponding to 11%) – N(Z corresponding to 8%).

本公式第一部分:利用excel中NORM.S.DIST这个公式,我们解得:58.48%

本公式第二部分,8%为均值,且为正态分布,则50%的概率落在均值两侧,所以,N(Z corresponding to 8%)=50%,

带入总公式:P(8% ≤ Portfolio return ≤ 11%) = 0.5848 - 0.50 = 0.0848 = 8.5%

老师,不知道从何入手,这是哪个知识点.考试中无法用Excel,怎么解答呢? 请问可以详细列一下解题步骤吗?谢谢