NO.PZ201803130100000101

问题如下:

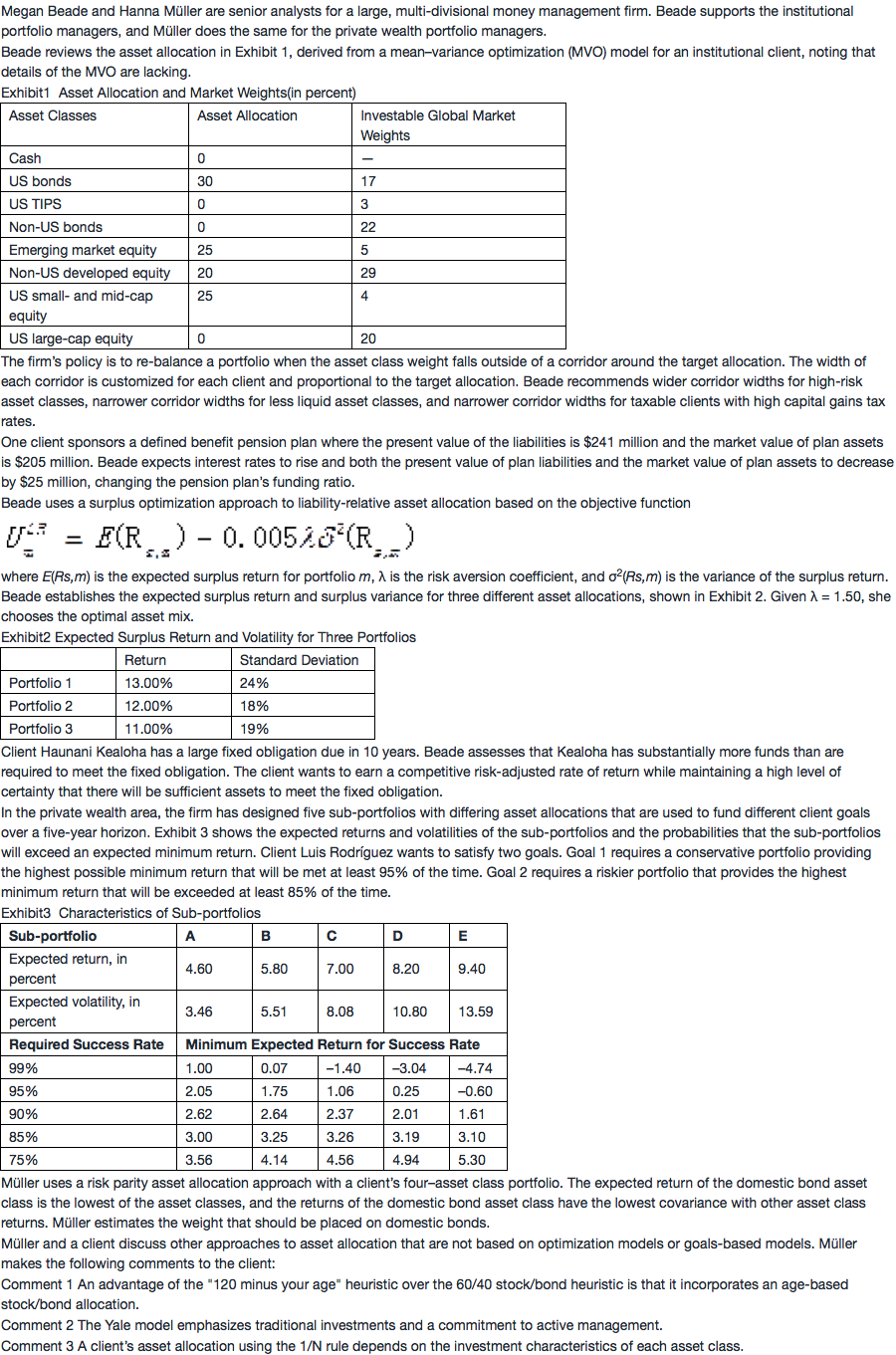

The asset allocation in Exhibit 1 most likely resulted from a mean–variance optimization using:

选项:

A.historical data.

B.reverse optimization.

C.Black–Litterman inputs.

解释:

A is correct.

The allocations in Exhibit 1 are most likely from an MVO model using historical data inputs. MVO tends to result in asset allocations that are concentrated in a subset of the available asset classes. The allocations in Exhibit 1 have heavy concentrations in four of the asset classes and no investment in the other four asset classes, and the weights differ greatly from global market weights. Compared to the use of historical inputs, the Black–Litterman and reverse-optimization models most likely would be less concentrated in a few asset classes and less distant from the global weights.

the Black–Litterman and reverse-optimization models

这两个模型不是解决MVO 对input敏感的问题吗?adding constraint 才是解决 concentrate的问题