NO.PZ2020033003000028

问题如下:

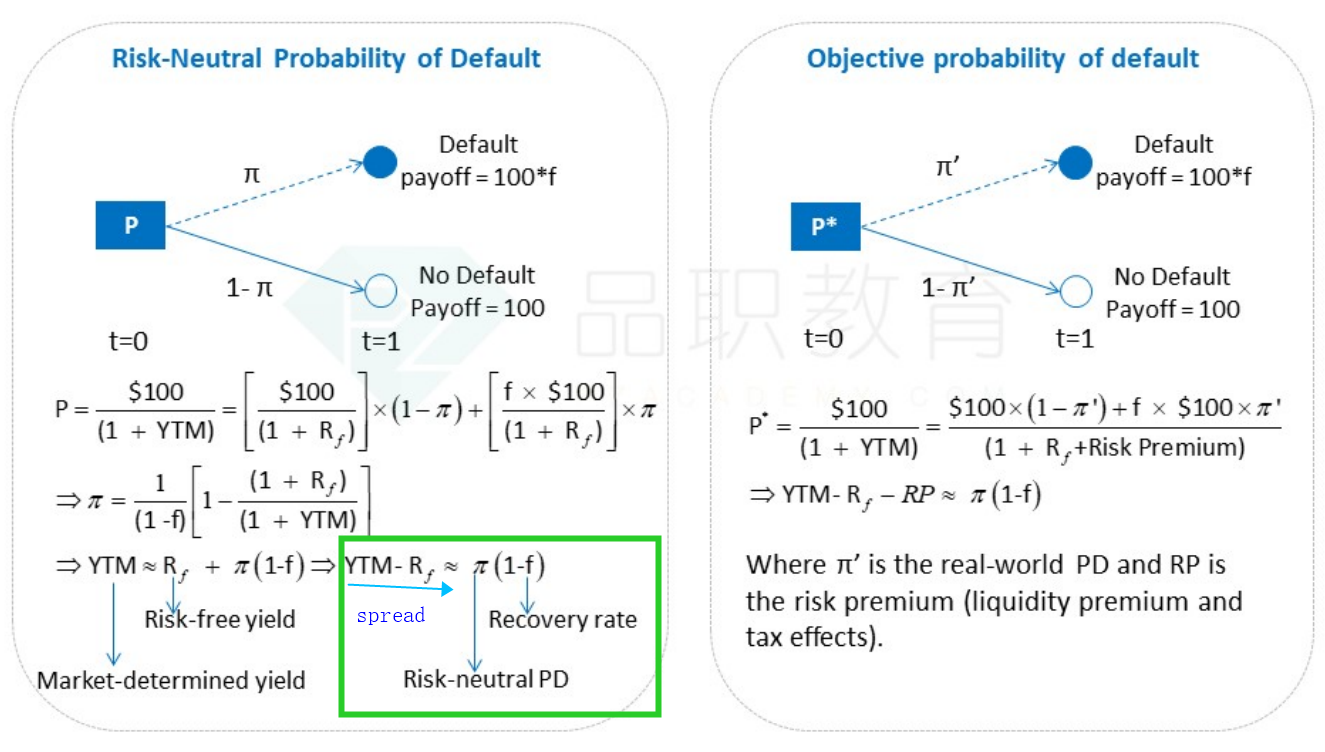

The analyst compares two bonds, one A-rated bond and the other BB-rated bond. The CDS spread of the two is 200 and 400 basis points respectively. According to the description of the internal rating report, the default probability of the two is 4 % And 13%, so which bond has higher recovery rate ?

选项:

A.A-rated bond.

B.BB-rated bond.

C.Equal.

D.Could not compare

解释:

B is correct.

考点:Hazard Rates-Risk-neutral Hazard Rates, Using CDS to estimate hazard rates

解析:近似计算Credit spread = (1 - RR) x (PD)

那么A级债的RR是50%,BB级债的RR是69%

BB级债的RR高。

这个公式的讲义在哪?