Taking the square root of 0.02395 gives σ(RDC) = 15.48%. If Aron executes the trade, the expected USD portfolio standard deviation equals the standard deviation of the EUR equity position, 15.00%. Therefore, the standard deviation of the portfolio decreases by 15.48% – 15.00% = 48 bps, which is more than Aron’s required decrease of 30 bps.

题目中说σ(RDC) = 15%,因为外汇风险已经被对冲If Aron executes the trade, the expected USD portfolio standard deviation equals the standard deviation of the EUR equity position, 15.00%

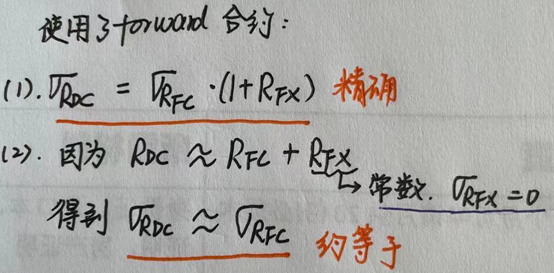

为什么课上何老师说外汇风险对冲时σ(RDC)=(1+RFX)σ(RFC) 呢

请问如何理解