NO.PZ2020033002000025

问题如下:

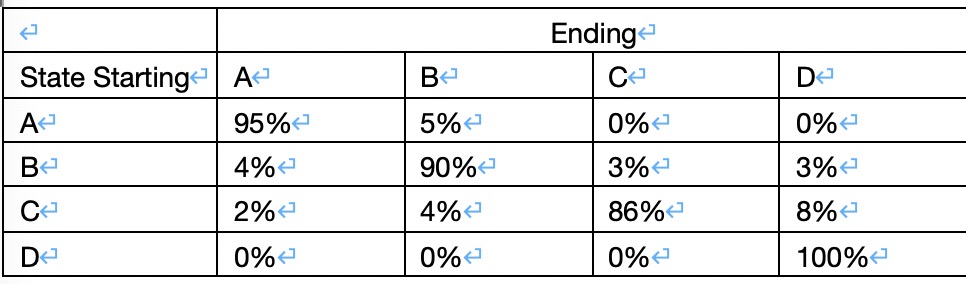

What is the probability that a firm currently rated B will default within two years, assuming a one-year credit rating transition matrix, as shown in the table below?

选项:

A.3%

B.5.94%

C.11%

D.14%

解释:

B is correct.

考点:Credit Transition Matrices

解析:

B第一年违约的概率是3%。

B第二年违约的概率分情况讨论

(1)第一年是B,第二年违约:90%*3%=2.7%

(2)第一年是C,第二年违约:3%*8%=0.24%

3%+2.7%+0.24%=5.94%

为什么不可能第一年是A,第二年违约?如果考虑此情况,算出的答案应该6.06%