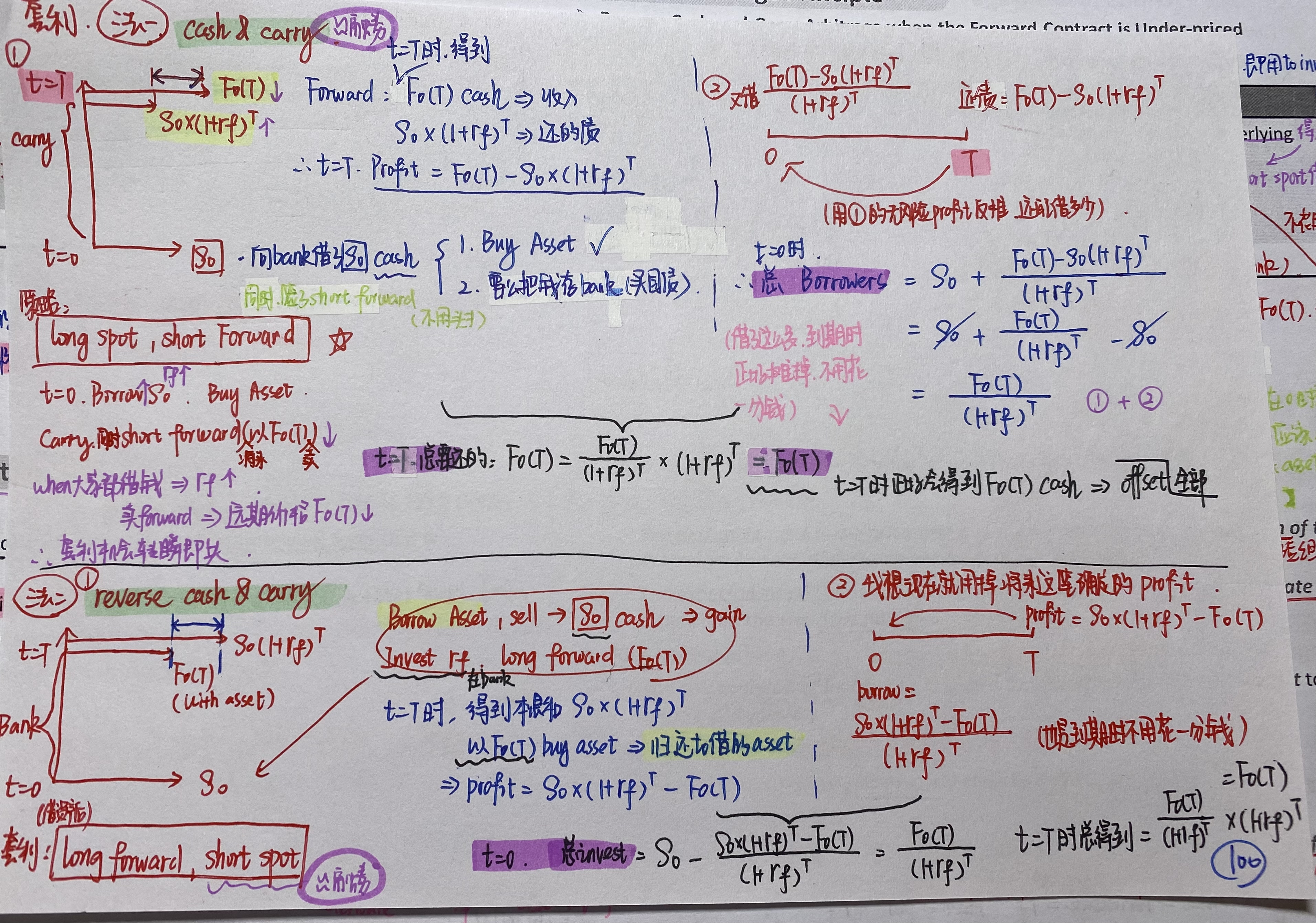

【forward arbitrary】

1.这两种套利情景是想说明的就是当F0(T)和从期初持有至最后这两种情况不等的时候可以无风险套利对吧?

2.这两种情况不管short还是long forward,默认在最初都是不用付成本的对吧,也就是0头寸?

【FRA settlement】

老师说只有value会决定profit,而price不能,但是远期的利润不是应该是St-F0(T)吗,这里的F0(T)不就是price?

【future pricing】

为什么FP上涨是说明赚钱了?FP不是在最初就固定好的价格F0(T)吗。

谢谢助教