问题如下:

Jane is asked to calculate the risk-neutral and real-world default probabilities of the bond A. She collected the following datas. The market price of the bond A with a face value of 100 is 95. The liquidity premium and credit risk premium are 2% and 1% respectively. The coupon rate of newly issued treasury bond is 2.5%. The expected inflation is 0.8%.

选项:

A.

B.

C.

D.

解释:

B is correct.

考点:Infer Credit Risk from Corporate Bond Prices

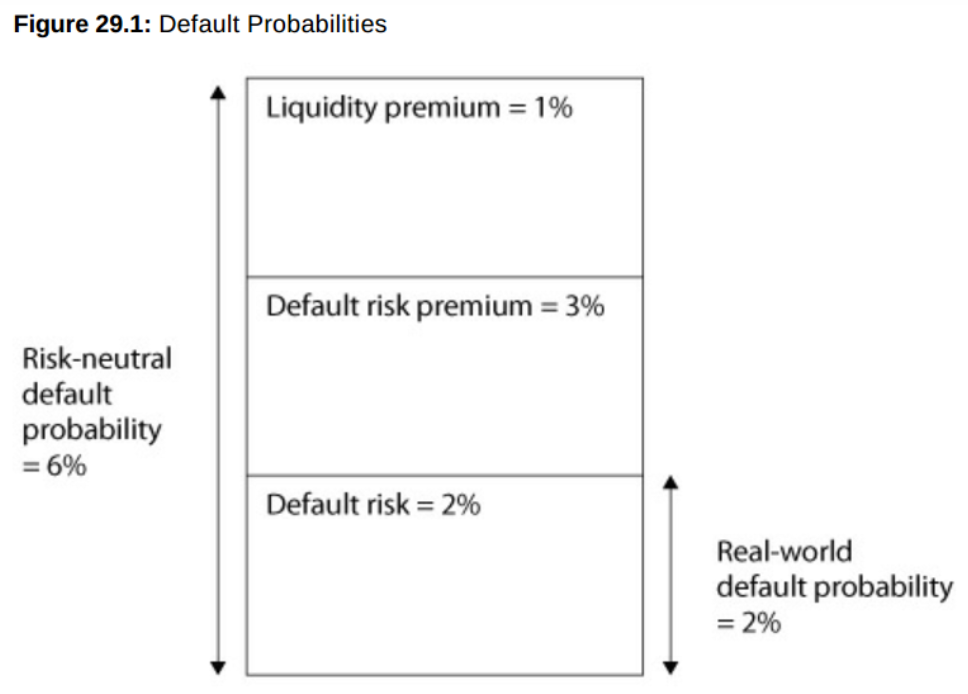

解析:risk-neutral default probability 100-95=5%

risk-neutral probability = real-world probability + credit risk premium + liquidity premium

real-world probability = 5% - 2%-1% = 2%

计算时为什么需要把credit risk的premium也减掉?记得讲义上是说把non-credit risk factors减掉即可