问题如下图:

选项:

A.

B.

C.

解释:

A和c都是一个意思啊,没有什么区别啊,最凸的不就有最大的系数吗?谢谢

NO.PZ2015121801000052问题如下With respeto utility theory, the most risk-averse investor will have infferencurve with the:A.most convexity.B.smallest intercept value.C.greatest slope coefficient.is correct.The most risk-averse investor hthe infferencurve with the greatest slope.老师 请问什么叫做slope coefficient呢,没看过这个概念。教材上写的greatest slope能懂 但是slope coefficient是另外的概念了吧

NO.PZ2015121801000052问题如下 With respeto utility theory, the most risk-averse investor will have infferencurve with the:A.most convexity.B.smallest intercept value.C.greatest slope coefficient.is correct.The most risk-averse investor hthe infferencurve with the greatest slope.a为什么不对,怎么看出来指一个投资者

NO.PZ2015121801000052 问题如下 With respeto utility theory, the most risk-averse investor will have infferencurve with the: A.most convexity. B.smallest intercept value. C.greatest slope coefficient. is correct.The most risk-averse investor hthe infferencurve with the greatest slope. 其中有一个回答就说“这题问的是most risk-averse investor的情况,他代表了极度厌恶风险的人群。所以对于这类人群,他们的无差异曲线不仅是凸的,而且凸的很明显;每一单位风险的增加会要求更高的收益率的增加。所以他们的无差异曲线斜率很大。”凸的很明显,不就表示Convexity很大么?就感觉 A和C表达是一个意思,麻烦老师再讲解一下

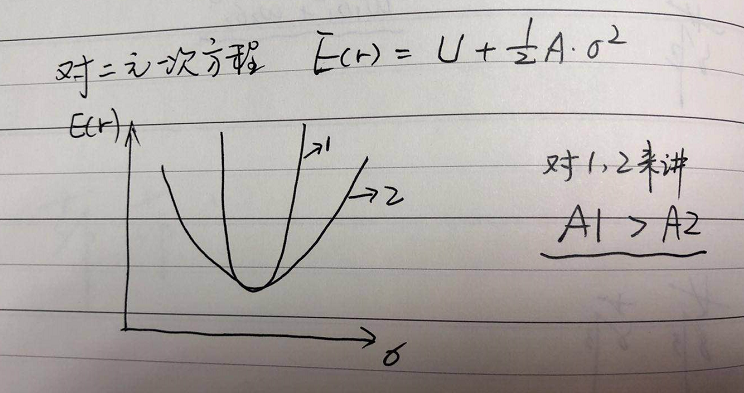

NO.PZ2015121801000052 问题如下 With respeto utility theory, the most risk-averse investor will have infferencurve with the: A.most convexity. B.smallest intercept value. C.greatest slope coefficient. is correct.The most risk-averse investor hthe infferencurve with the greatest slope. 看了之前的解答,还是有点疑惑,a里面的most convexity难道不是这个最风险厌恶的投资者跟其他投资者比起来他是最convexity的吗?感觉之前的回答里老师的说的不是很清楚,麻烦老师讲一下。丹丹_品职答疑助手 · 超过 1 年前嗨,从没放弃的小努力你好同学你好,可以借用效用理论的公式U=E(r)-0.5*A(stanrv)^2,所以对于同一个投资者convexity是相同的

NO.PZ2015121801000052 能否下,谢谢助教!