NO.PZ201809170400000603

问题如下:

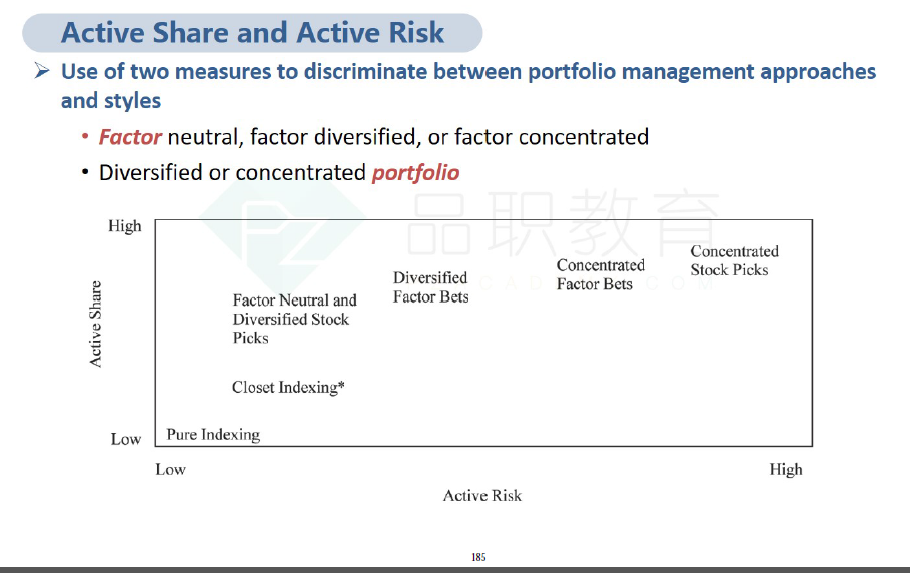

Manager B’s portfolio is most likely consistent with the characteristics of a:

选项:

A. pure indexer.

B. sector rotator.

C. multi-factor manager.

解释:

C is correct. Most multi-factor products are diversified across factors and securities and typically have high active share but have reasonably low active risk (tracking error), often in the range of 3%. Most multi-factor products have a low concentration among securities in order to achieve a balanced exposure to risk factors and minimize idiosyncratic risks. Manager B holds a highly diversified portfolio that has balanced exposures to rewarded risk factors, a high active share, and a relatively low target active risk—consistent with the characteristics of a multi-factor manager.

答案裡的 Multi factor model 是low concentration of stock 是什麼意思呢 不是每一個風險因子也有各自一類的股票代表這個因子嗎 那應該每一個因子也是high concentration的stock和high exposure to that risk? High active share 和 low active risk在這裡的multi factor model 的理解 是和benchmark 不一樣權重 但用的股票還是高度correlation?