NO.PZ201702190300000107

问题如下:

Based on Exhibits 2 and 3, and assuming annual compounding, the per share value of Troubadour’s short position in the TSI forward contract three months after contract initiation is closest to:

选项:

A. $1.6549.

B. $5.1561.

C. $6.6549.

解释:

C is correct.

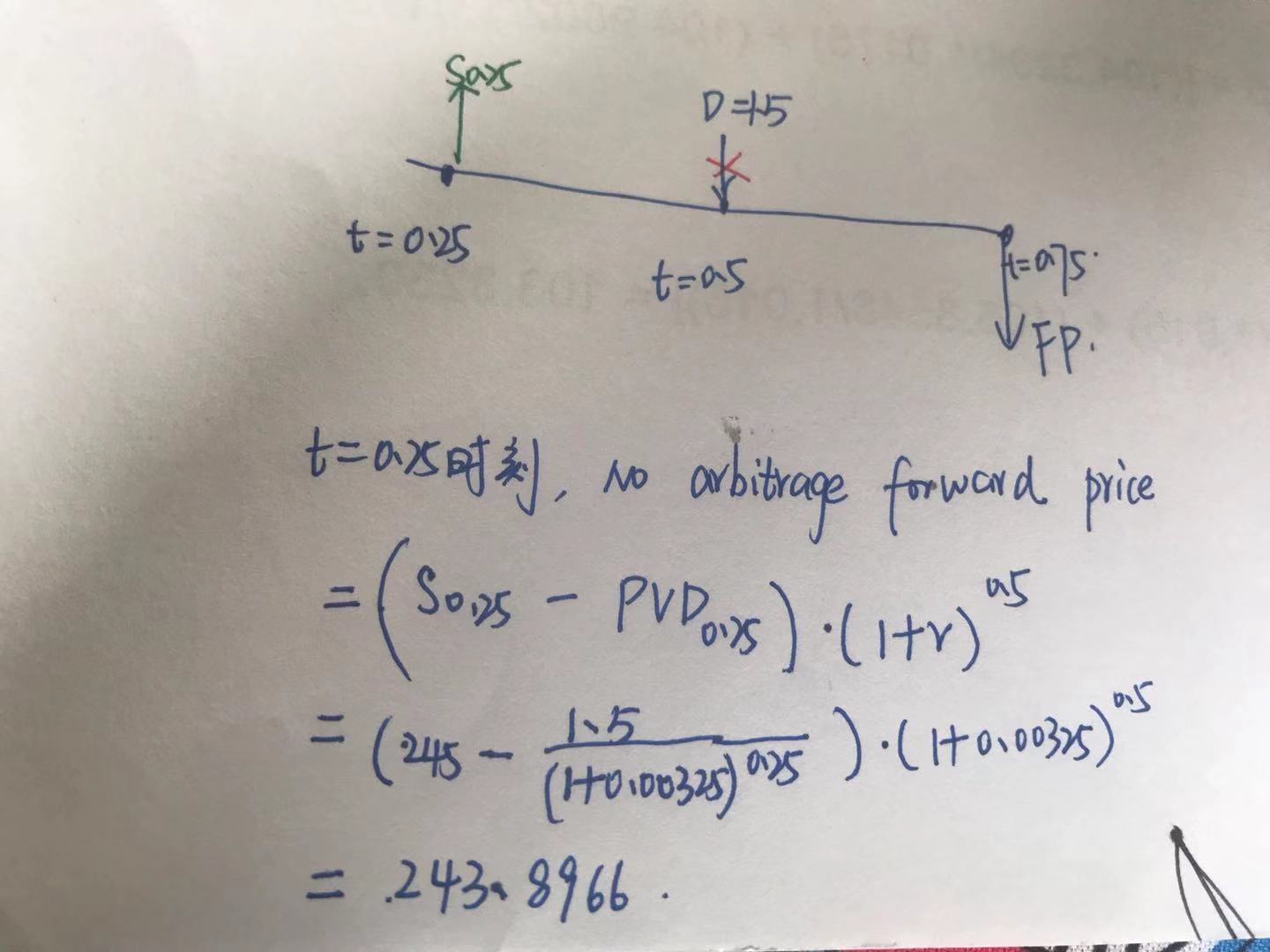

The no-arbitrage price of the forward contract, three months after contract initiation, is

F0.25(T) = FV0.25,T(S0.25 + θ.25 –γ0.25)

F0.25(T) = [$245 + 0 - $1.50/(1 + 0.00325)(0.5 - 0.25)](1 + 0.00325)(0.75 -0.25) = $243.8966

Therefore, from the perspective of the long, the value of the TSI forward contract is

V0.25(T)=PV0.25,T [F0.25(T) – F0(T)]

V0.25(T) = ($243.8966- $250.562289)/(1 + 0.00325)0.75 - 0.25 =-$6.6549

Because Troubadour is short the TSI forward contract, the value of his position is a gain of $6.6549.

在long position中 T时刻有权以fp买入资产,说明还未持有该资产,因此div取不到 那么short position对应的不是应该在T时刻卖出,而现在是持有该资产的吗?既然持有div为什么是减去呢 难道所有头寸都是无法取得div吗?