NO.PZ201809170400000302

问题如下:

The Mackenzie Education Foundation funds educational projects in a four-state region of the United States. Because of the investment portfolio’s poor benchmark-relative returns, the foundation’s board of directors hired a consultant, Stacy McMahon, to analyze performance and provide recommendations.

McMahon meets with Autumn Laubach, the foundation’s executive director, to review the existing asset allocation strategy. Laubach believes the portfolio’s underperformance is attributable to the equity holdings, which are allocated 55% to a US large-capitalization index fund, 30% to an actively managed US small-cap fund, and 15% to an actively managed developed international fund.

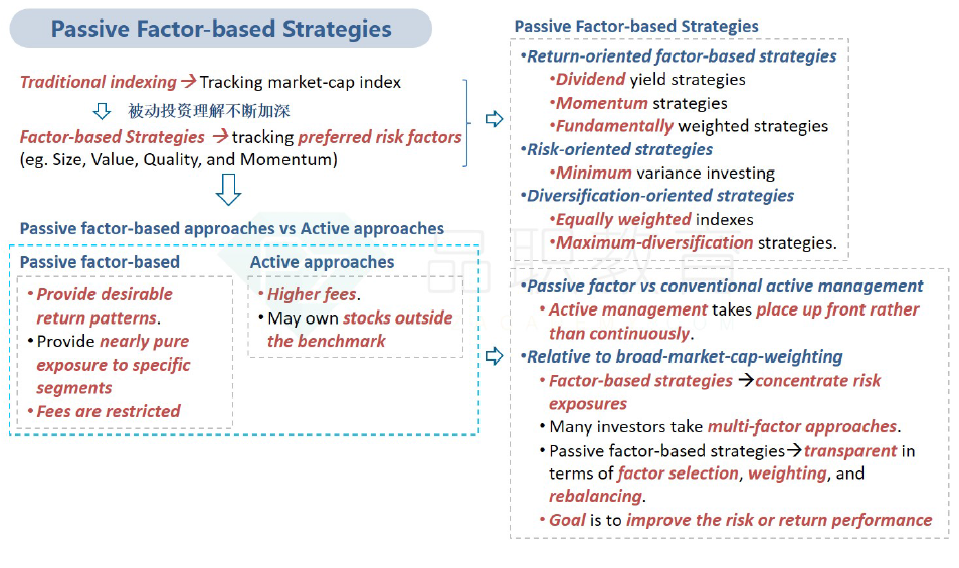

Laubach states that that the board is interested in following a passive approach for some or all of the equity allocation. In addition, the board is open to approaches that could generate returns in excess of the benchmark for part of the equity allocation. McMahon suggests that the board consider following a passive factor-based momentum strategy for the allocation to international stocks.

McMahon observes that the benchmark used for the US large-cap equity component is a price-weighted index containing 150 stocks. The benchmark’s Herfindahl–Hirschman Index (HHI) is 0.0286.

McMahon performs a sector attribution analysis based on Exhibit 1 to explain the large-cap portfolio’s underperformance relative to the benchmark.

The board decides to consider adding a mid-cap manager. McMahon presents candidates for the mid-cap portfolio. Exhibit 2 provides fees and cash holdings for three portfolios and an index fund.

The international strategy suggested by McMahon is most likely characterized as:

选项:

A. risk based.

B. return oriented.

C. diversification oriented.

解释:

B is correct. McMahon suggests that the foundation follow a passive factor-based momentum strategy, which is generally defined by the amount of a stock’s excess price return relative to the market during a specified period. Factor-based momentum strategies are classified as return oriented.

Passive factor based 和active factor based 的分別是什麼呢? 就是像 和 不像 index 的分別嗎 像就passive? 謝謝