NO.PZ2020042003000081

问题如下:

The following statements are about the

yield curve strategies named carry trade, which of the following statements

about carry trade is NOT correct?

选项:

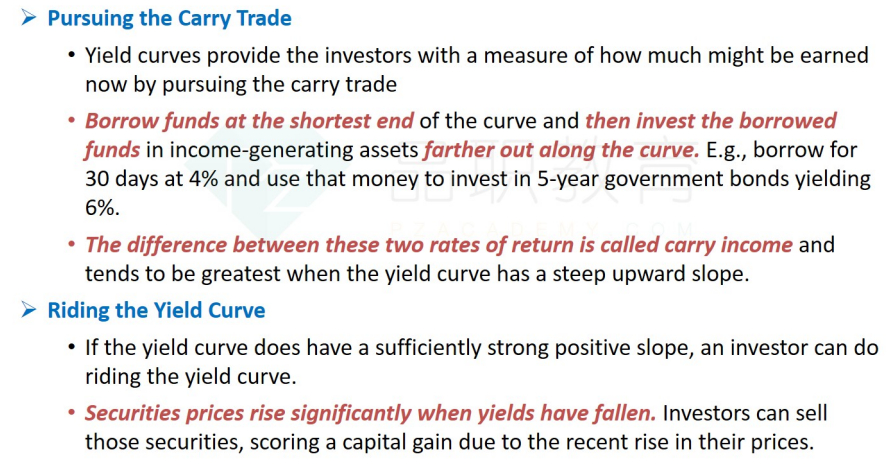

A. when the yield curve is upward sloping, borrow

funds at the shortest end of the curve and then invest the borrowed funds in

income-generating assets farther out along the curve.

B. The

difference between these short-term and long-term rates of return is called

carry income.

C. By doing carry trade, investors are expecting

securities prices rise significantly when yields have fallen and sell those

securities, scoring a capital gain due to the recent rise in their prices.

D. The

return of carry trade tends to be greatest when the yield curve has a steep

upward slope

解释:

考点:对Maturity Management Tools的理解

答案:C

解析:

选项C的表述错误,Carry

trade期望赚取的是息差,C选项描述的是Riding the

yield curve预期赚取的收益。

能解释一下?????