NO.PZ201602060100000803

问题如下:

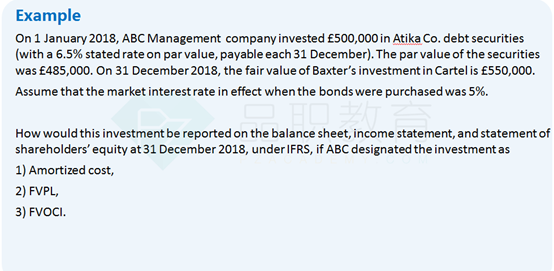

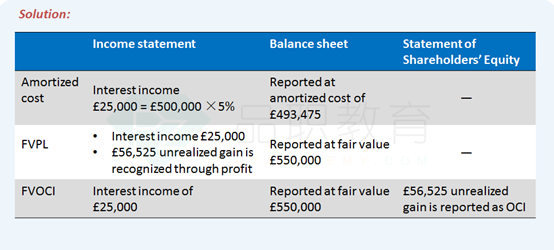

Burton Howard, CFA, is an equity analyst with Maplewood Securities. Howard is preparing a research report on Confabulated Materials, SA, a publicly traded company based in France that complies with IFRS 9. As part of his analysis, Howard has assembled data gathered from the financial statement footnotes of Confabulated’s 2018 Annual Report and from discussions with company management. Howard is concerned about the effect of this information on Confabulated’s future earnings.

Information about Confabulated’s investment portfolio for the years ended 31 December 2017 and 2018 is presented in Exhibit 1. As part of his research, Howard is considering the possible effect on reported income of Confabulated’s accounting classification for fixed income investments.

Exhibit 1. Confabulated’s Investment Portfolio (€ Thousands)

*All securities were acquired at par value.

In addition, Confabulated’s annual report discusses a transaction under which receivables were securitized through a special purpose entity (SPE) for Confabulated’s benefit.

Compared to Confabulated’s reported interest income in 2018, if Dumas had been classified as FVPL, the interest income would have been:

选项:

A.lower.

B.the same.

C.higher.

解释:

B is correct.

The coupon payment is recorded as interest income whether securities are amortized cost or FVPL. No adjustment is required for amortization since the bonds were bought at par.

考点:Financial asset 的会计计量

解析:

平价发行债券没有摊销问题,interest income就等于收到的coupon payment,不管分类为amortized资产还是FVPL,interest income都是一样的。

划分为FVPL的话,债券FV的变动不应该确认在IS吗,这样不会增加income嘛?