问题如下:

Which of the following statement is not

correct?

选项:

A.

We can use the difference between the bid and

ask prices as a cost of liquidity.

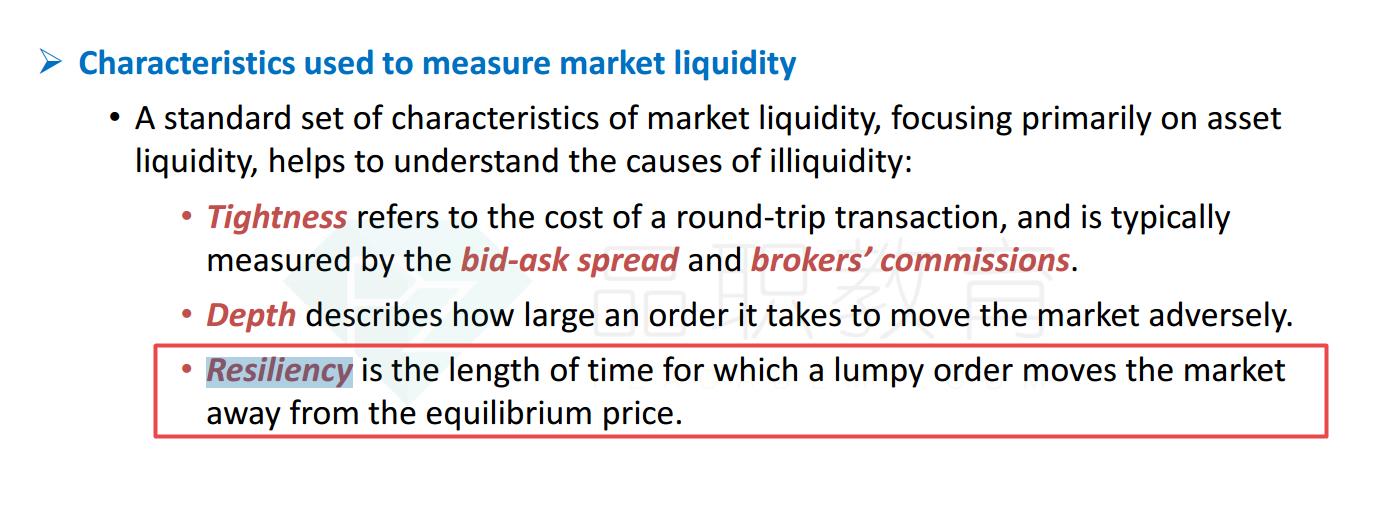

B.

When we measure the market liquidity, tightness

refers to the cost of a round-trip transaction, and is typically measured by

the bid-ask spread and brokers’ commissions.

C.

When we measure the market liquidity, depth

describes the length of time for which a lumpy order moves the market away from

the equilibrium price.

D. If the bid-ask spread were a constant, then going long at the offer and short at the bid would be a predictable cost of doing the trade.

解释:

考点:对Transaction liquidity risk measurement的理解

答案: C选项表述错误,因此本题选C。

解析:

C选项表述错误,Depth正确的表述为: Depth describes how large an order it takes to move the market

adversely.

C选项描述的情景属于Resiliency:

resiliency is the length of time for which a lumpy order moves the market away

from the equilibrium price.

想问下这是在讲义的第几页?