NO.PZ201712110200000105

问题如下:

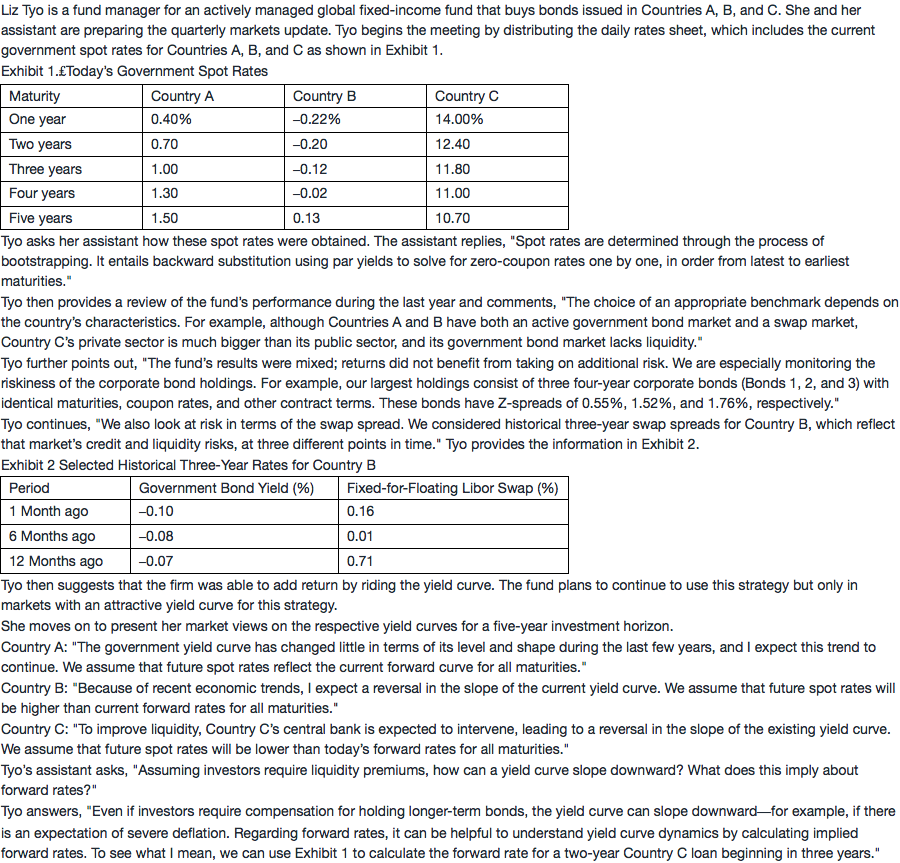

Based on Exhibit 1 and Tyo’s expectations, which country’s term structure is currently best for traders seeking to ride the yield curve?

选项:

A.Country A

B.Country B

C.Country C

解释:

A is correct.

Country A’s yield curve is upward sloping—a condition for the strategy—and more so than Country B’s.

C国为什么不选呢?经过政府干预后不也恢复正常了吗?spot rate比forward rate不就是正常的吗?