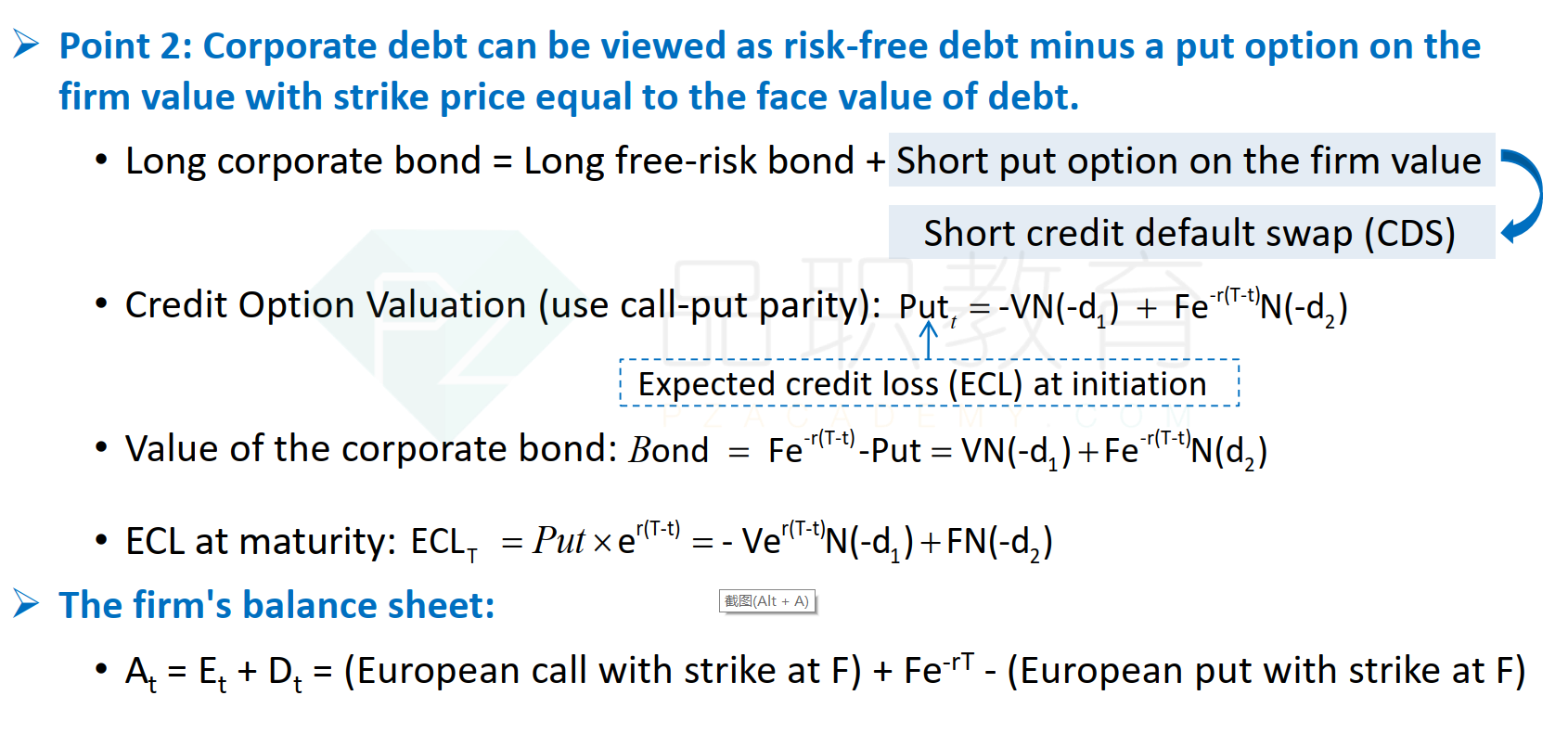

NO.PZ2020033003000104

问题如下:

Adam is asked to estimate the value of firm A’s equity under the Merton framework.

1)The value of firm A's asset is180.

2)Risk-free rate of 5%.

3)The firm issues one-year zero interest bonds with a face value of 100.

4)The value of a European put option on the firm's asset is 3.50 and the strike price is 100.

选项:

A.$95.12.

B.$91.62.

C.$92.12

D.$88.38.

解释:

D is correct.

考点:Merton Model

解析:无风险债券的现值=100*e^(-0.05)=95.12

公司债券的价值=95.12-3.50=91.62

公司的股权价值=180-91.62=88.38

公司债券的价值=95.12-3.50=91.62