NO.PZ2020033003000078

问题如下:

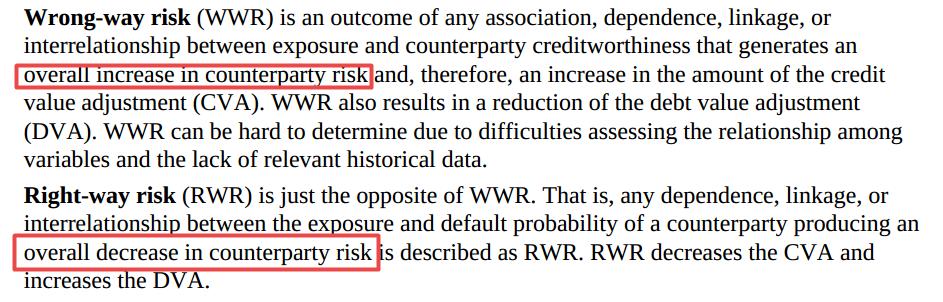

Which of the following statement about Right-Way Risk(RWR) and Wrong-Way Risk(WWR) is not correct?

选项:

A.In the 2008 financial crisis, the CDSs buyer is facing WWR.

B.The depreciation of the foreign currency leads to losses in foreign currency transactions and increases the probability of counterparty default,the foreign currency inverstor is facing WWR.

C.A long call option is facing RWR if both the risk exposure and counterparty default probability decrease.

D.A long put option is facing WWR, if the risk exposure and counterparty default probability both increase.

解释:

B is correct.

考点:Wrong-Way Risk Vs. Right-Way Risk

解析:外币贬值导致外币投资的亏损,此时我方收益减少或者损失增加,在对方看来我方的违约率可能会增加。

换言之此时exposure和违约概率不会同时变大,B错误。

那如果A和B同时减少不能说明二者正相关

A和B一增一减 可以说明二者负相关吗?

如题,谢谢~