NO.PZ2019070901000097

问题如下:

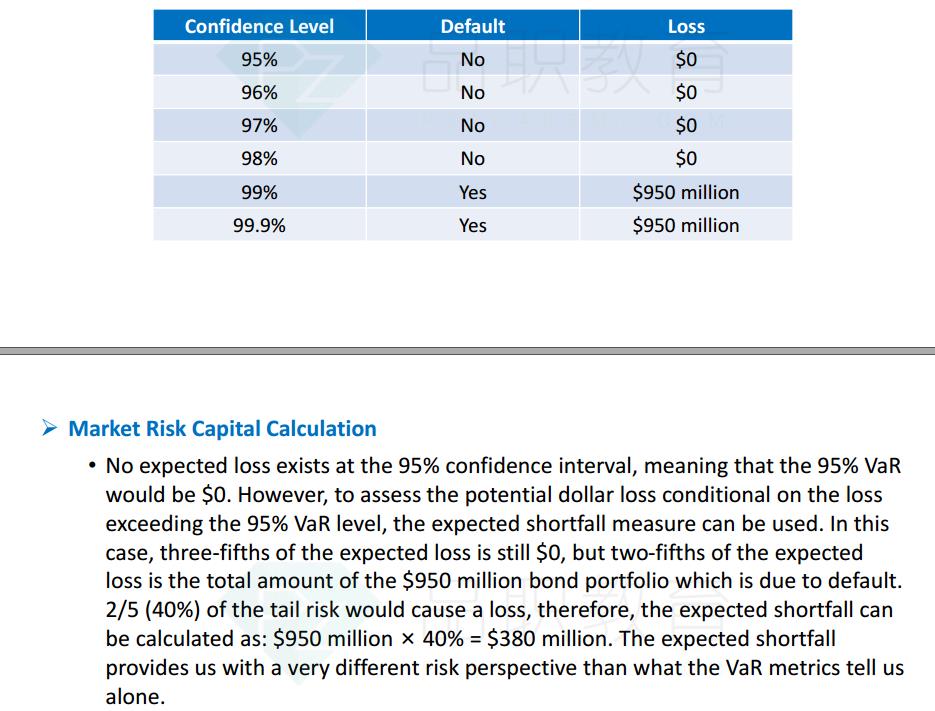

A bond portfolio has 950million in asset and a probability of default of 0.7% with 0% recovery rate. what is the difference between the 99% VaR and 99% expected shortfall ?

选项:

A.The 99%VaR and the 99% expected shorfall both equal 0.

B.The 99%VaR equals $950 million, while the 99% expected shortfall euquals 665million.

C.The 99% VaR equals 0, while the expected shortfall equals $665 million.

D.The 99%VaR and the 99% expected shorfall both equal 950million.

解释:

C is correct.

考点:VaR和ES度量

解析:损失概率为0.7%时,位于99%VaR的尾部,所以VaR的1%的位置显示的风险值为0,但是尾部的70%都是损失部分,也就是950million的损失。所以expected shortfall等于950million*70%=665million.

答案的70%是哪来的,题目没给。