NO.PZ2020033002000050

问题如下:

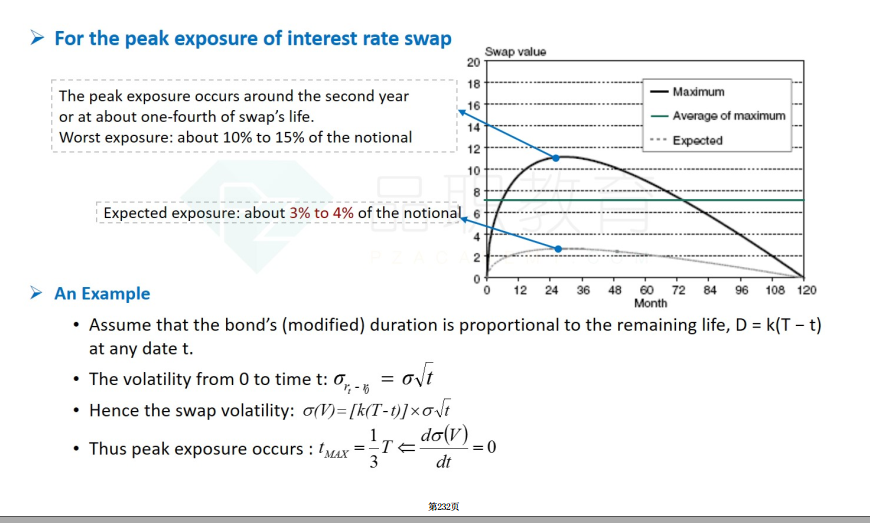

Ace Bank entered into a fixed-for-floating interest rate swap that starts today and ends in six years. If the duration of this position is proportional to the time to maturity and all changes in the yield curve are parallel shifts, and that the volatility of interest rates is proportional to the square root of time. When would the maximum potential exposure be reached?

选项:

A.Today B.In two years

C.In four years

D.In six years

解释:

B is correct.

考点:Credit exposure

解析:

t=T/3 时达到peak exposure

有没有什么情况,会改变1/3T这个结论?谢谢!