NO.PZ2020021204000017

问题如下:

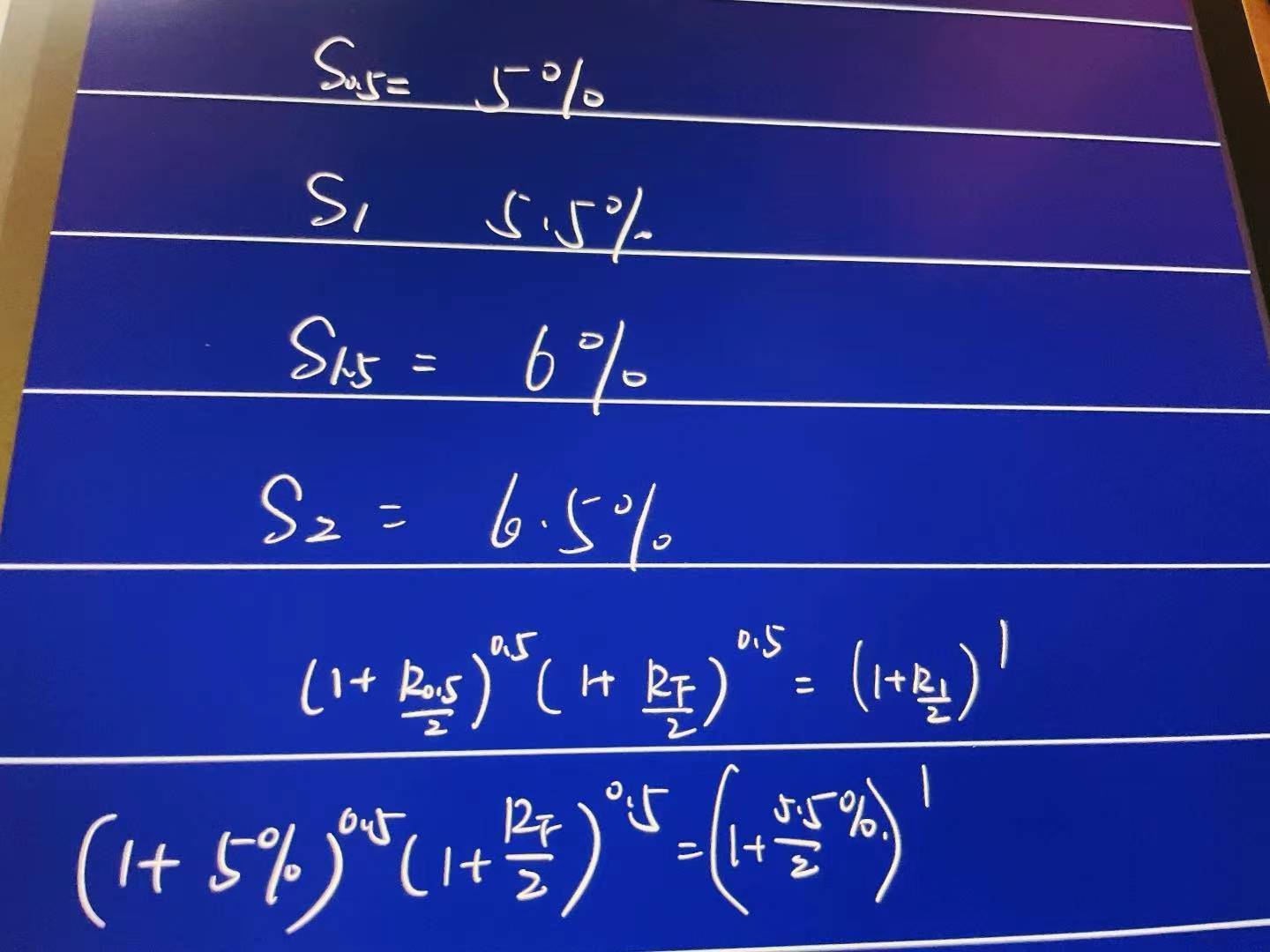

The six-month, 12-month, 18-month, and 24-month zero rates are 5%, 5.5%, 6%, and 6.5%, what are the (semi-annually compounded) forward rates for a six-month periods beginning in six, 12, and 18 months?

选项:

解释:

The forward rates are

2 X ( 1.02752 /1.025-1) = 0.060012

2 X ( 1.033 /1.02752- 1) = 0.070037

2 X ( 1.03254 /1.033 - 1)= 0.080073

If all rates were continuously compounded, the forward rates would be 6%, 7%, and 8%. Because we are dealing with a semi-annually compounded rate, they are slightly different: 6.0012%, 7 .0037%, and 8.0073%.

这是代T1*R1+(T2-T1)Rf=T2*R2的公式吗?

老师能看一下我写的计算吗,错哪?以及这样的方程怎么按计算器啊,用计算器的时候都需要先吧(1+5%)0.5先运算完再记下来,再算右边的式子,可以指点一下怎么按计算器吗,看了计算器的视频也没明白。