NO.PZ2018070201000084

问题如下:

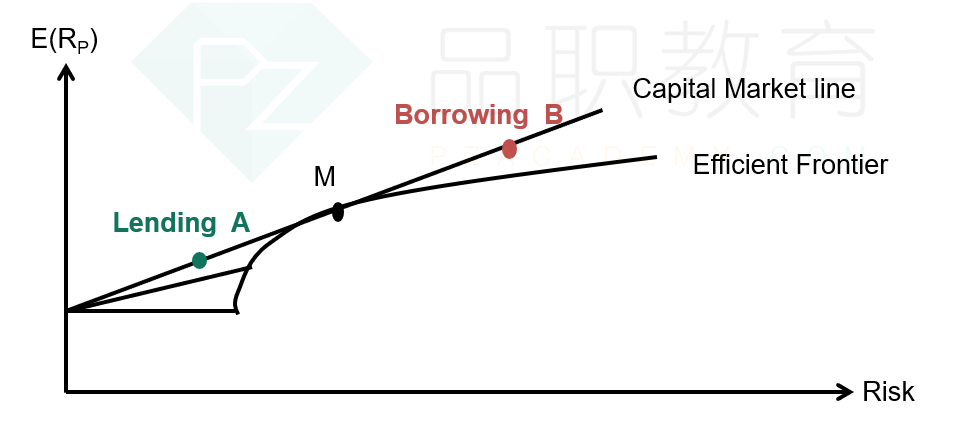

Which of the following statements about lending portfolio is correct?

选项:

A. The portfolio return of a combination between risk-free assets and the market portfolio is less than the return of the market portfolio.

B. The portfolio return of a combination between risk-free assets and the market portfolio is higher than the return of the market portfolio.

C. The portfolio return of a combination between risk-free assets and the market portfolio is equal to the return of the market portfolio.

解释:

A is correct.

In the CML, a lending portfolio shows that the portfolio return of a combination between risk-free assets and the market portfolio is less than the return of the market portfolio.

如上方问题,点在左边合风险资产的组合收益不是更大吗