NO.PZ2019070901000087

问题如下:

Avocado Bank calculates market risk capital through an internal model approach to meet the requirements of the 1996 Amendment to the Basel Accord. They found 8 exceptions when backtesting the 99%,one-day var against the actual losses over the last 250 trading days. Based on the number of expctions, which of the following multiplicative factor should be seted ?

选项:

A.between 2.1 and 2.9.

B.3.

C.4.

D.between 3.1 and 3.9.

解释:

D is correct.

考点:multiplicative factor

解析:Avocado Bank 需要将它计算出来的250个交易日中99%的one-day VaR与同一时期的实际损失进行比较,以确定multiplicative factor。 如果实际损失大于估计损失,记录一次例外。

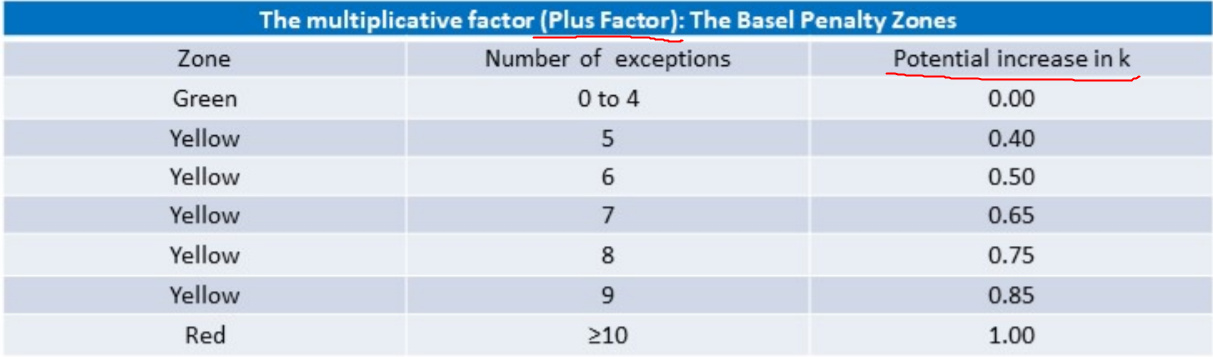

例外次数对应的multiplicative factor如下:

小于5时,multiplicative factor为3,

5到9次的例外对应3.1到3.9这个区间(五个数字分别对应3.4,3.5,3.65,3.75和3.85)

大于等于10次的例外系数为4。

强化串讲,P13页那个multiplicative factor penalty zoom里面0到4 对应的是0, 5对应的是0.4.。。。。。。这个表格和答案解析里面的表格又什么不一样吗,解析里面的表格在讲义里面哪里呢