NO.PZ201512300100001207

问题如下:

7. Under Scenario 1, the intrinsic value per share of the equity of Amersheen is closest to:

选项:

A.R13.29.

B.R15.57.

C.R16.31.

解释:

As the multistage residual income model results in an intrinsic value of R16.31.

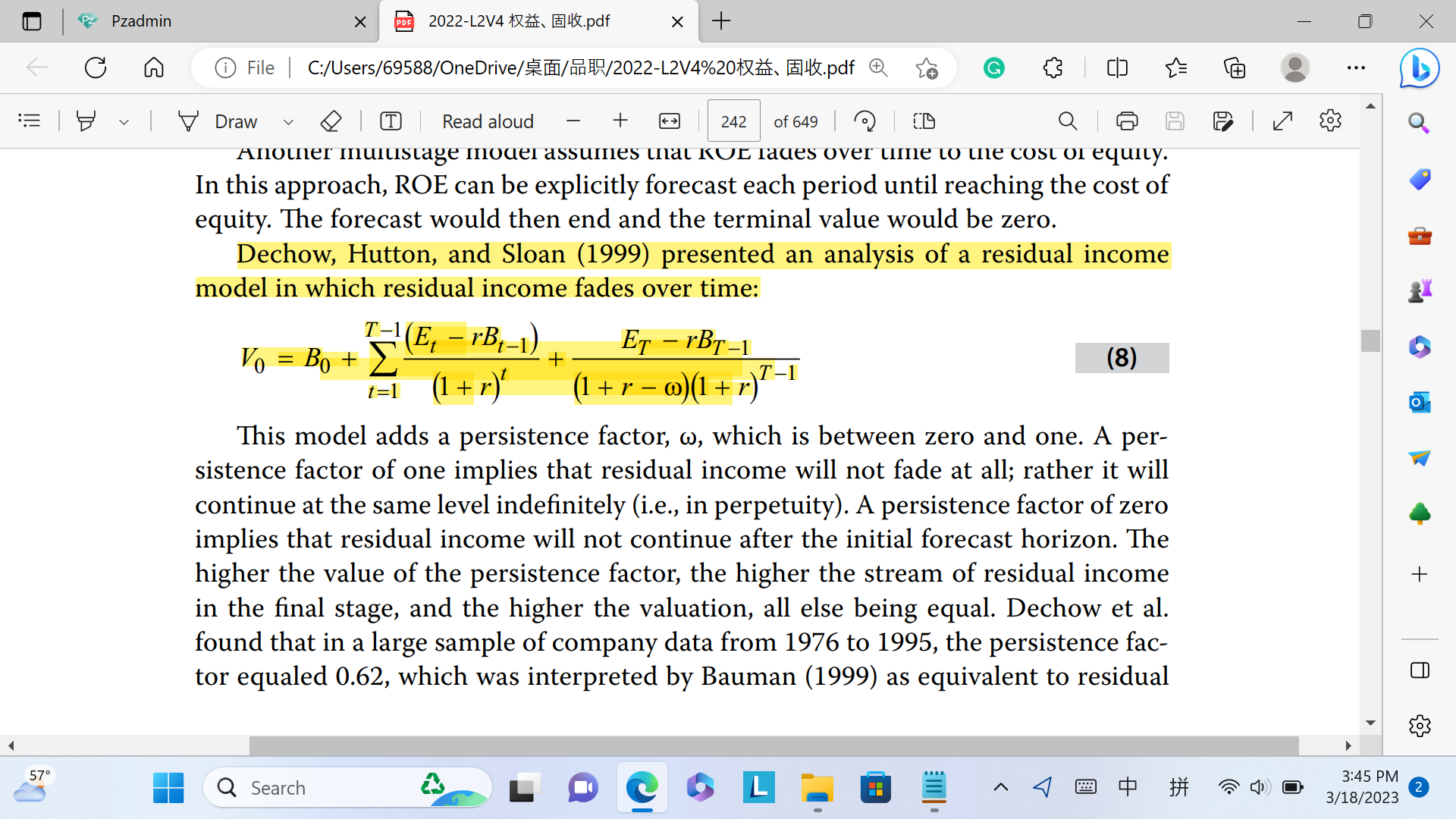

This variation of the multistage residual income model, in which residual income fades over time, is:

where

The first step is to calculate residual income per share for years 2012

ROE = earnings / book value

Growth rate = ROE × retention rate

Retention rate = 1

Book valuet= book valuet

Residual income per share = EPS

Equity charge per share = book value per sharet× cost of equity

Using the residual income per share for 2015 of R1.608, the second step is to calculate the present value of the terminal value:

PV of Terminal Value =

Then, intrinsic value per share is:

PV of Terminal Value =

R1.6081+0.10-0.70(1.10)3=R3.0203

Then, intrinsic value per share is:

V0=R7.60+R2.52(1.10)+R2.31(1.10)2+R1.98(1.10)3+R3.0203=R16.31

您好,根据公式算出的PVRI2015=RI2015*w/(1+re-w)=1.6018*0.7/0.4=2.81不是3.0203。请问是哪里算错了吗?谢谢!